Southeast Asia is the connective tissue of SEA Weekly. This page brings together the themes that move across borders: manufacturing shifts, logistics upgrades, consumer demand, tourism recovery, and the regional sports calendar.

ASEAN’s Q3 supply-chain map is now priced by recovery time and auditability more than nominal cheapness, and the hierarchy is already visible in this week’s corridor reporting.

Singapore is anchoring ASEAN supply chain resilience by turning port, warehouse, air-cargo and finance integration into paid optionality as Q3 volatility rises.

Capital is available at the institutional level but not reaching ASEAN’s SME manufacturers — and Q3 freight costs are stretching cash cycles just as credit access tightens.

AI adoption in ASEAN trade finance is accelerating at the fraud and compliance layer — but the $2.5 trillion gap is unchanged because AI cannot yet reach the SME tier where the data infrastructure required for credit models barely exists.

Vietnam’s export recovery is real, but logistics costs at 16–20% of GDP mean every freight-rate swing hits exporters harder here than anywhere else in ASEAN — and the US-Iran peace deal won’t deliver a clean cost reset.

ASEAN loan growth numbers are hiding a deeper liquidity stress in the deposit base — and when liquidity tightens, loan growth is the last metric to turn.

Singapore’s institutional premium model and Malaysia’s consumer ecosystem model represent two fundamentally different answers to the same question — how to turn digital payments ubiquity into profit — and the gap between them is reshaping fintech strategy across ASEAN.

Timor-Leste has ASEAN membership, a credible sovereign wealth fund, and a functioning PPP — the question is whether these can attract sufficient private capital before the Petroleum Fund depletion timeline binds.

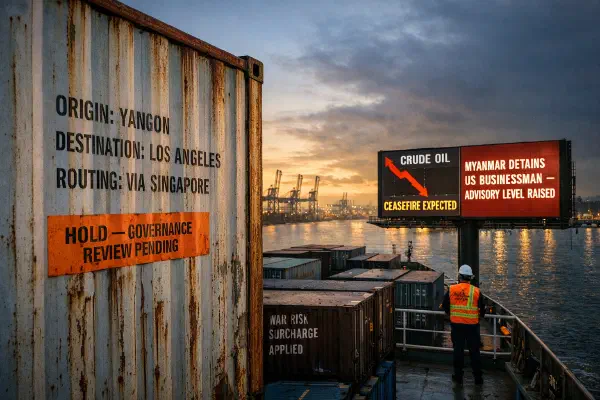

The US-Iran peace deal is the best supply chain news ASEAN frontier markets have had all year. But governance risk is now repricing upward on its own axis, and the net premium may not fall as much as logistics alone would suggest.

Indonesia’s banks are in their best-ever shape, but rupiah defense is creating a credit transmission failure that will define ASEAN lending patterns through H2 2026.

Brunei is taking the right institutional steps toward post-hydrocarbon diversification, but the pieces aren’t yet connected, the sovereign wealth lever remains under-deployed, and the Iran war windfall is both the best enabler and the biggest trap.

ASEAN’s fiscal divergence in 2026 is not primarily about who exports oil. It’s about who made subsidy reform calls in the quiet years before the shock — and Malaysia and the Philippines are holding more fiscal cards going into H2 than Indonesia or Thailand.

Laos inflation is running at 9% because the country is structurally pinned: it produces 83% of its energy from hydropower yet cannot keep Électricité du Laos solvent, and it has zero domestic refining capacity yet imports 97% of its fuel from Thailand.

Southeast Asia’s garment sector is facing a reckoning where the savings of low-cost manufacturing are being erased by “Logistics Entropy”—the combined cost of surging fuel, worker safety crises, and unpredictable US trade policy. Cambodia is repositioning as a “stable but expensive” hub, while Myanmar is increasingly viewed as a “no-go” zone for all but the most risk-tolerant.

Record remittance volumes mask a quality story that matters far more for Philippines household consumption in 2026 — the sectoral and geographic composition of OFW sending patterns is quietly reshaping what families can actually spend.