Cambodia is a rapidly industrialising economy of around 17 million people, with Phnom Penh emerging as a significant commercial hub and Siem Reap drawing millions of visitors to the Angkor temple complex. The garment and footwear sector drives merchandise exports, while Special Economic Zones along the Thai and Vietnamese borders attract diversified light manufacturing. A young, mobile-first population is accelerating adoption of digital payments and consumer finance at a pace that outstrips much of the region.

ASEAN’s Q3 supply-chain map is now priced by recovery time and auditability more than nominal cheapness, and the hierarchy is already visible in this week’s corridor reporting.

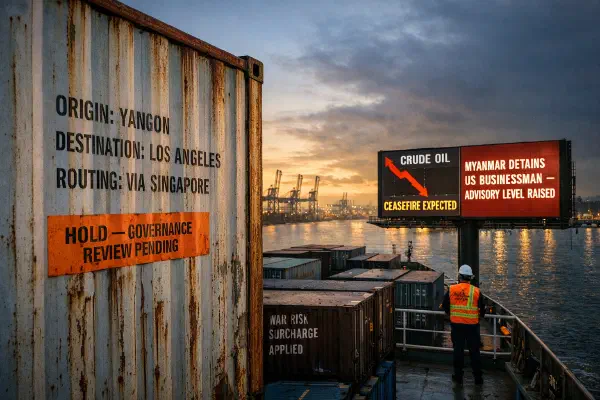

Myanmar remains cheaper on wages, but Cambodia is winning 2026 garment orders because buyers can still audit, insure and ship its corridor with less risk.

ASEAN’s logistics and freight signals are now the most informative leading indicators for H2 growth — they move weeks ahead of trade volumes, months ahead of GDP revisions, and the differential across economies is already in this season’s order books.

Cambodia and Laos are both under garment export pressure in H2 2026, but from opposite directions — and the window for H2 order booking is open right now.

Laos is becoming more important to ASEAN’s power grid, but export scale alone will not repair the balance sheet unless Laos captures more value from transmission, PPAs, and domestic grid reform.

Cambodia’s manufacturing volume headlines look strong, but the factories that survive H2 are those with BFC-audited buyers and non-commodity order books — not those that frontloaded before tariff uncertainty resolved.

Airlines across Southeast Asia are reshaping regional mobility by deploying new aircraft to secondary cities, bypassing saturated megahubs ahead of the Q3 peak.

Philippine aviation demand is surging but infrastructure constraints and visa barriers mean the benefits are increasingly captured by ASEAN competitors with better capacity to serve high-yield travellers.

The US-Iran peace deal is the best supply chain news ASEAN frontier markets have had all year. But governance risk is now repricing upward on its own axis, and the net premium may not fall as much as logistics alone would suggest.

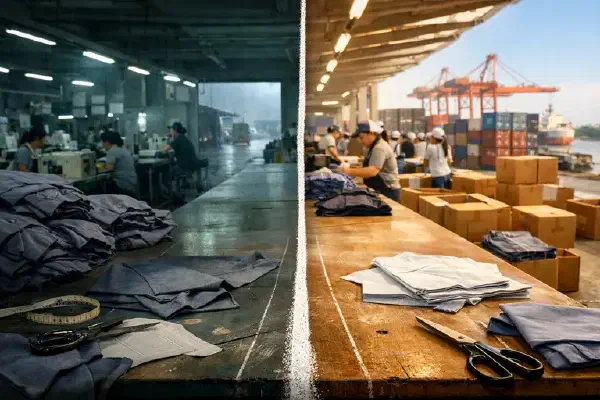

Southeast Asia’s garment sector is facing a reckoning where the savings of low-cost manufacturing are being erased by “Logistics Entropy”—the combined cost of surging fuel, worker safety crises, and unpredictable US trade policy. Cambodia is repositioning as a “stable but expensive” hub, while Myanmar is increasingly viewed as a “no-go” zone for all but the most risk-tolerant.

The tariff anniversary week that mattered wasn’t for what it revealed about factories. It was for what it revealed about the alternative architecture Southeast Asia has been quietly building.