The most valuable seat in ASEAN aviation this quarter may be the one no traveler ever books. It sits below the cabin floor.

For most of the past year, airlines in Southeast Asia could pretend passenger planning and freight planning were adjacent problems. Q3 2026 ends that separation. Air cargo demand is still firm, belly capacity is tighter than it looks, and fuel and freight disruption are forcing carriers to decide which routes deserve scarce aircraft, scarce schedule slack, and scarce operational confidence.

The cabin is selling tickets. The belly is deciding the route.

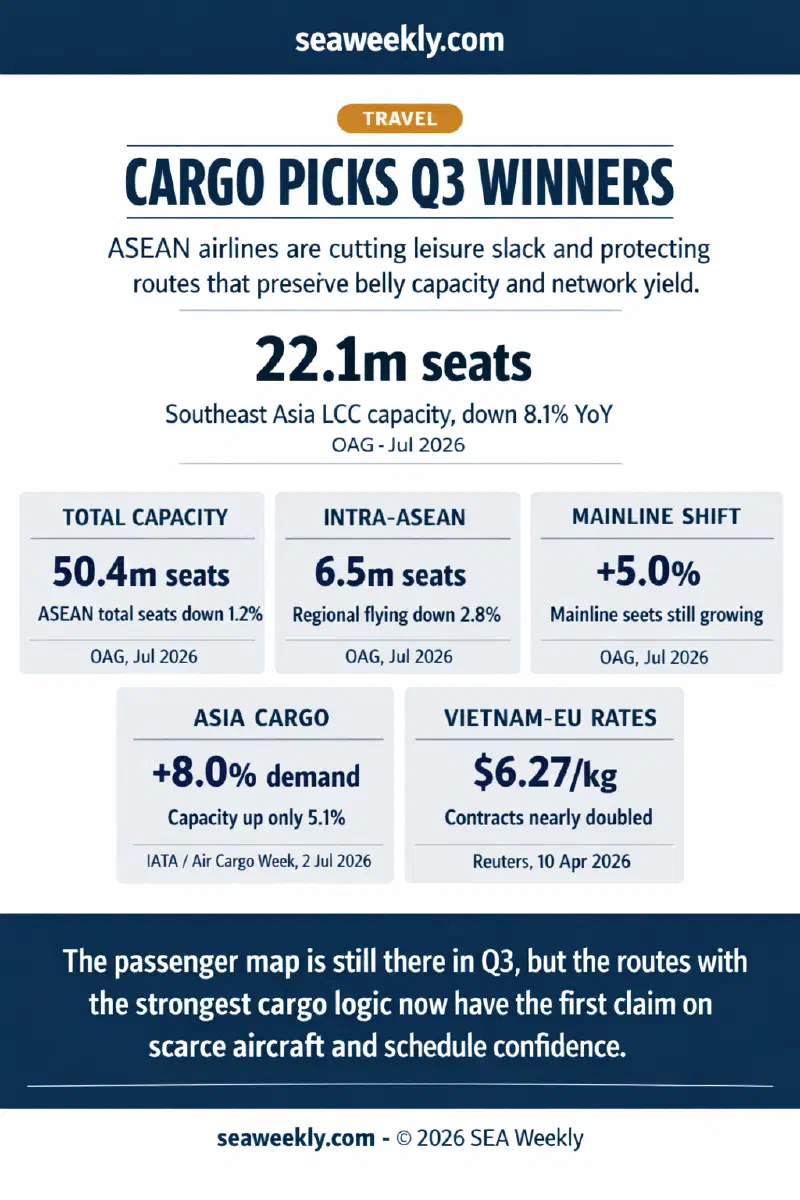

The first fact to get clear is that cargo has stopped behaving like filler revenue. DHL’s June market update said global air-cargo volumes rose 4% year on year in May 2026, while freighter capacity grew 7% but passenger belly capacity still fell 2% (DHL, June 2026). IATA’s May data, reported by Air Cargo Week, showed Asia-Pacific demand up 8.0% against only 5.1% capacity growth, with Asia-North America volumes up 19.9% (Air Cargo Week, July 2, 2026).

That does not mean ASEAN airlines are turning themselves into cargo carriers. It means a passenger flight with useful belly space now carries a more strategic second job than it did a year ago. When lower-deck capacity is scarce, aircraft assignment stops being a pure leisure-demand question.

Reuters made that pressure visible in March and April. The March 13 freight report showed South Asia-Europe rates up 70% to USD 4.37 per kilogram from USD 2.57, with carriers rerouting around Gulf disruption and in some cases accepting payload restrictions on direct flights (Reuters, March 13, 2026). By April 10, Reuters was reporting that long-term Vietnam-Europe contract rates had nearly doubled to USD 6.27/kg and that cargo capacity into the Middle East had shrunk by more than 50% on an annual basis over two weeks (Reuters, April 10, 2026).

Once belly space becomes that valuable, passenger route planning changes tone. The question is no longer only “Where can we sell seats?” It becomes “Which flights still earn their keep across passengers, connectivity, and freight at the same time?”

ASEAN’s July seat map already shows the trade-off.

OAG’s July 2026 Southeast Asia briefing is the clearest read on how that trade-off is appearing in schedule data. Total regional capacity is down 1.2% year on year to 50.4 million seats. Within-Southeast-Asia flying, the part of the map most closely associated with casual regional mobility and shorter discretionary trips, is down 2.8% to 6.5 million seats (OAG, July 2026).

The carrier mix is even more revealing. Mainline airlines now hold 56% of Southeast Asia capacity, up to 28.3 million seats and growing 5.0% year on year. Low-cost carriers have fallen to 22.1 million seats, down 8.1%, with AirAsia down 21.9%, Lion Air down 20.9%, and Thai AirAsia down 22.3%. Yet Vietnam Airlines remains the region’s largest airline at 2.81 million seats, Singapore Airlines is up 4.9%, and Cebu Pacific is up 8.3% (OAG, July 2026).

This is not a clean story of weak passenger demand. It is a hierarchy shift. Airlines are protecting the parts of the network that do more than one job: trunk routes, hub-feed routes, and longer-haul flying where freight value or network value is stronger. OAG’s destination data makes the same point from another angle. Capacity from Southeast Asia to Europe and North America rose 10.7% and 11.5% respectively, while capacity to the Middle East fell 3.3% and within-ASEAN flying contracted harder than the overall market (OAG, July 2026).

The uncomfortable implication for travelers is that Q3 schedules are being shaped at least partly by the needs of exporters and network managers, not only by the desires of holidaymakers.

In ASEAN, cargo pressure is operational before it is theoretical.

The pressure shows up in decisions passengers rarely notice until the timetable has already thinned out. Reuters reported on April 7 that Vietnam Airlines had cut 23 domestic flights per week to conserve fuel. The same report said AirAsia X was loading extra fuel in Malaysia before flying into Vietnamese airports because uplift there was limited (Reuters, April 7, 2026). Those are passenger-airline scheduling choices being made inside a logistics squeeze.

Dimerco’s July Asia-Pacific freight report gives the airport-side explanation. Bangkok and Manila terminal congestion are extending door-to-door lead times, several Southeast Asian airfreight markets remain tight on U.S. and Europe lanes, and the Southwest Monsoon is layering weather risk on top of an already unforgiving quarter (Dimerco, July 1, 2026). In that environment, an airline cannot look at bookings alone and add a marginal frequency wherever a fare sale seems to work. It has to ask whether the airport can turn the aircraft cleanly, whether fuel planning has become more conservative, and whether the route supports a larger network logic.

This is why the line between a passenger route and a cargo route is getting blurrier. A widebody departure from a major ASEAN hub now carries three businesses at once: people, baggage, and time-sensitive trade.

Vietnam is the clearest clue, not the whole story.

Vietnam is not the whole ASEAN aviation market, but it offers the sharpest illustration of how export logic can influence route decisions. CEVA’s June 24 launch of a three-times-weekly Hanoi-Chicago Boeing 777 freighter tells you something important even though it is not a passenger service: manufacturers in northern Vietnam are paying for guaranteed long-haul air capacity because reliability has become strategically important again (AJOT, June 24, 2026). Once that kind of cargo demand exists in a market, passenger planners cannot treat adjoining hub routes as interchangeable commodities.

That is what makes this week’s story different from the one I wrote on June 19 about ASEAN aviation route competition. That earlier brief argued that airlines were bypassing megahubs and fighting over secondary-city access (SEA Weekly, June 19, 2026). That remains true. But the July twist is harsher: not every city-pair gets equal protection when fuel costs stay high, freight rates stay elevated, and the lower deck suddenly matters more.

Why AirAsia’s pivot matters even if it is not the only example.

AirAsia’s July 9 corporate reset is useful because it supplies the language airlines use when they stop chasing seat volume for its own sake. The group said its new structure is designed to optimize the network, strengthen operations, and improve connectivity across short- and medium-haul flying (AirAsia Newsroom, July 9, 2026). That is not the vocabulary of indiscriminate expansion. It is the vocabulary of network triage.

Cargo is not the only reason for that shift. Fuel discipline, aircraft availability, monsoon disruption, and cost-of-living pressure all matter too. But cargo is part of the logic. When Asia freight rates remain 30% to 50% above last year’s levels and belly capacity is tighter than the headline passenger market suggests, the route with stronger connection value and stronger freight optionality is easier to defend than the route that sells only cheap seats.

What travelers will actually feel in Q3.

Travelers are unlikely to describe this as a cargo story. They will feel it as thinner schedule padding and more ruthless route prioritization.

The first symptom is less slack on secondary or purely leisure-heavy flying. If an airline has to decide where to place a constrained aircraft, it will prefer a route that feeds a hub bank, protects a trunk connection, or better supports high-value freight over one that depends only on seasonal discount demand.

The second symptom is that mainline hubs gain relative importance. Singapore Changi remains the region’s busiest airport at 3.56 million seats, while Hanoi is one of the few top-10 airports showing fast growth (OAG, July 2026). Those hubs are not simply places passengers pass through. They are platforms where airlines can monetize connectivity above and below the cabin floor.

The third is that frequency decisions become less forgiving. Once a route has to justify itself through passenger yield, freight contribution, and operational resilience all at once, it becomes harder for airlines to indulge weaker links in the network.

There is a cultural cost to that, and a travel desk should name it. One of the quiet democratic gains of the past decade in Southeast Asia has been the sense that more of the region became casually reachable: an extra weekend connection, an easier secondary-city trip, a less punishing itinerary through the archipelago. Q3’s freight competition does not reverse that story. But it does reveal how dependent that freedom has become on an airline cost structure that is more freight-exposed than most passengers understand.

The passenger map is still there in Q3, but the routes with the strongest cargo logic now have the first claim on scarce aircraft and schedule confidence.

References:

- OAG (July 2026). “Southeast Asia aviation market briefing.” https://www.oag.com/south-east-asia-aviation-flight-data (Accessed July 16, 2026)

- DHL (June 2026). “Air Freight Market Update.” https://www.dhl.com/us-en/home/global-forwarding/latest-news-and-webinars/air-freight-market-update.html (Accessed July 16, 2026)

- Air Cargo Week (July 2, 2026). “Air cargo demand rises 6 percent in May despite Middle East disruption.” https://aircargoweek.com/air-cargo-demand-rises-6-percent-in-may-despite-middle-east-disruption/ (Accessed July 16, 2026)

- Reuters (March 13, 2026). “Air freight rates soar as Middle East conflict blocks trade routes.” https://www.reuters.com/world/middle-east/air-freight-rates-soar-middle-east-conflict-blocks-trade-routes-2026-03-13/ (Accessed July 16, 2026)

- Reuters (April 7, 2026). “Asian airlines trim schedules and carry extra fuel as supplies tighten.” https://www.reuters.com/business/energy/asian-airlines-trim-schedules-carry-extra-fuel-supplies-tighten-2026-04-07/ (Accessed July 16, 2026)

- Reuters (April 10, 2026). “Shippers weigh unusual routes as high air cargo rates, ocean gridlock persist.” https://www.reuters.com/business/energy/shippers-weigh-unusual-routes-high-air-cargo-rates-ocean-gridlock-persist-2026-04-10/ (Accessed July 16, 2026)

- Reuters (April 9, 2026). “British Airways cuts Middle East flights, shifts capacity to Asia and Africa.” https://www.reuters.com/world/middle-east/british-airways-cuts-middle-east-flights-shifts-capacity-asia-africa-2026-04-09/ (Accessed July 16, 2026)

- Dimerco (July 1, 2026). “Asia Pac Freight Report: July 2026.” https://dimerco.com/news-press/asia-pac-freight-report-july-2026/ (Accessed July 16, 2026)

- AJOT (June 24, 2026). “CEVA boosts Asia Pacific-U.S. air cargo with two charters connecting Vietnam, China to U.S.” https://www.ajot.com/news/ceva-boosts-asia-pacific-u.s-air-cargo-with-two-charters-connecting-vietnam-china-to-u.s (Accessed July 16, 2026)

- AirAsia Newsroom (July 9, 2026). “AirAsia enters new era as AirAsia Group Berhad, advancing its vision to become the world’s first low-cost network carrier.” https://newsroom.airasia.com/news/2026/7/9/airasia-enters-new-era-as-airasia-group-berhad-advancing-its-vision-to-become-the-worlds-first-low-cost-network-carrier (Accessed July 16, 2026)

- SEA Weekly (June 19, 2026). “What’s driving ASEAN aviation route competition before peak months?” https://seaweekly.com/posts/2026-06-19-asean-aviation-route-competition/ (Accessed July 16, 2026)