Laos is a landlocked nation of around 7 million people sitting at the geographic heart of mainland Southeast Asia, bordered by China, Vietnam, Cambodia, Thailand, and Myanmar. The opening of the China–Laos Railway in 2021 transformed the country’s transit potential, enabling rail-linked trade flows between Kunming and Vientiane and reducing the cost of moving goods across the subregion. Hydropower exports to neighbouring countries provide a stable hard-currency revenue stream, while the Mekong river corridor and UNESCO-listed Luang Prabang sustain a growing eco-heritage tourism sector.

Cambodia and Laos are both under garment export pressure in H2 2026, but from opposite directions — and the window for H2 order booking is open right now.

Laos is becoming more important to ASEAN’s power grid, but export scale alone will not repair the balance sheet unless Laos captures more value from transmission, PPAs, and domestic grid reform.

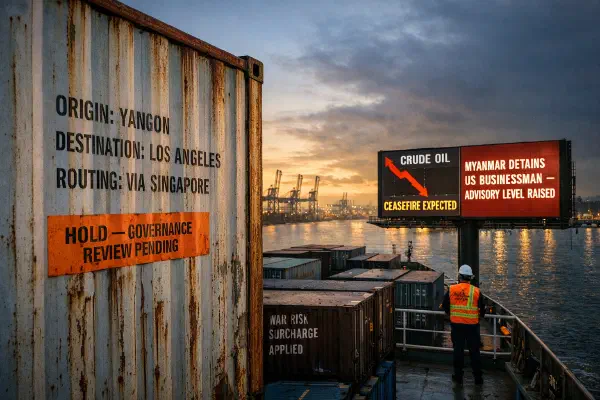

The US-Iran peace deal is the best supply chain news ASEAN frontier markets have had all year. But governance risk is now repricing upward on its own axis, and the net premium may not fall as much as logistics alone would suggest.

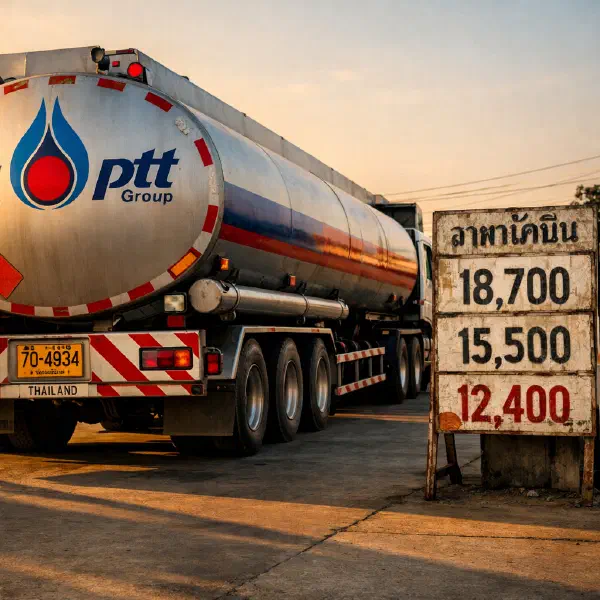

Laos inflation is running at 9% because the country is structurally pinned: it produces 83% of its energy from hydropower yet cannot keep Électricité du Laos solvent, and it has zero domestic refining capacity yet imports 97% of its fuel from Thailand.