Southeast Asia is the connective tissue of SEA Weekly. This page brings together the themes that move across borders: manufacturing shifts, logistics upgrades, consumer demand, tourism recovery, and the regional sports calendar.

ASEAN’s Q3 supply-chain map is now priced by recovery time and auditability more than nominal cheapness, and the hierarchy is already visible in this week’s corridor reporting.

Singapore is anchoring ASEAN supply chain resilience by turning port, warehouse, air-cargo and finance integration into paid optionality as Q3 volatility rises.

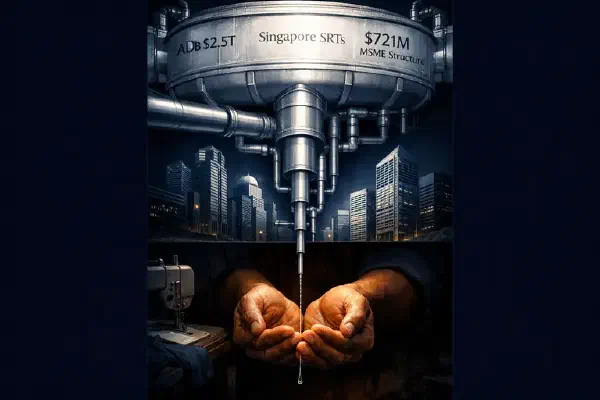

Capital is available at the institutional level but not reaching ASEAN’s SME manufacturers — and Q3 freight costs are stretching cash cycles just as credit access tightens.

AI adoption in ASEAN trade finance is accelerating at the fraud and compliance layer — but the $2.5 trillion gap is unchanged because AI cannot yet reach the SME tier where the data infrastructure required for credit models barely exists.

Three simultaneous repricing events are settling ASEAN’s H2 capital map. Thailand has emerged as the surprise winner — not through tourism or domestic consumption, but through AI data centre infrastructure. Indonesia’s governance premium is now a hard market fact. Singapore’s institutional moat is actively widening. The H2 growth competition was won on institutional quality, not growth rate.

Malaysia is pushing up the value ladder into semiconductor IP and advanced design while Vietnam is racing to close a localisation deficit in volume electronics manufacturing. Both strategies are legitimate. The competitive zone where they genuinely collide — advanced PCB, compound subassembly, precision electronics components — is where global supply chain investment decisions will be made and where both countries’ industrial policy ambitions are most directly tested.

Singapore is winning ASEAN capital-flow positioning because Brunei has hard-currency credibility and sovereign wealth, but not the intermediation layer global money pays for.

Laos is becoming more important to ASEAN’s power grid, but export scale alone will not repair the balance sheet unless Laos captures more value from transmission, PPAs, and domestic grid reform.

Commercial operators are retreating from ASEAN sports rights. Telecoms and state broadcasters are filling the gap. The structural repricing of sports sponsorship is now underway — and it will reshape who sponsors ASEAN sport, at what price, and through what channel.

Cambodia’s manufacturing volume headlines look strong, but the factories that survive H2 are those with BFC-audited buyers and non-commodity order books — not those that frontloaded before tariff uncertainty resolved.

Thailand is actively raising prices across airlines and hotels and demand holds. The Philippines’ high per-visitor yield is a supply constraint, not a strategy — and the distinction is the most important signal in ASEAN tourism right now.

This week’s ASEAN signal is not about growth; it is about systems integration — the markets where fintech infrastructure and industrial throughput are closing into a single investable stack are attracting better capital, on better terms, than those where the two layers are still moving on separate calendars.

Airlines across Southeast Asia are reshaping regional mobility by deploying new aircraft to secondary cities, bypassing saturated megahubs ahead of the Q3 peak.

Philippine aviation demand is surging but infrastructure constraints and visa barriers mean the benefits are increasingly captured by ASEAN competitors with better capacity to serve high-yield travellers.

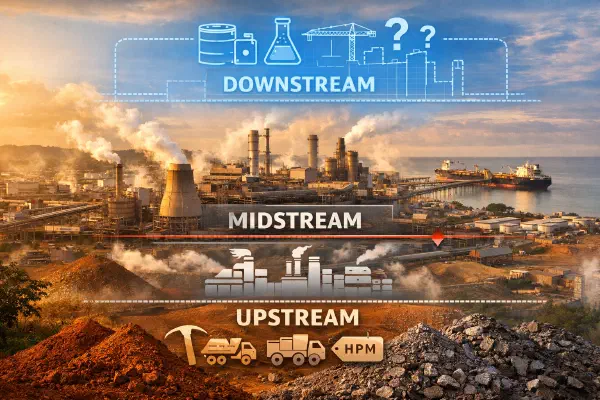

Indonesia’s nickel value capture in 2026 is not a single story of triumph or capture — it is a three-layer contest between the state, Chinese processors, and new entrants, and each layer has a different winner.