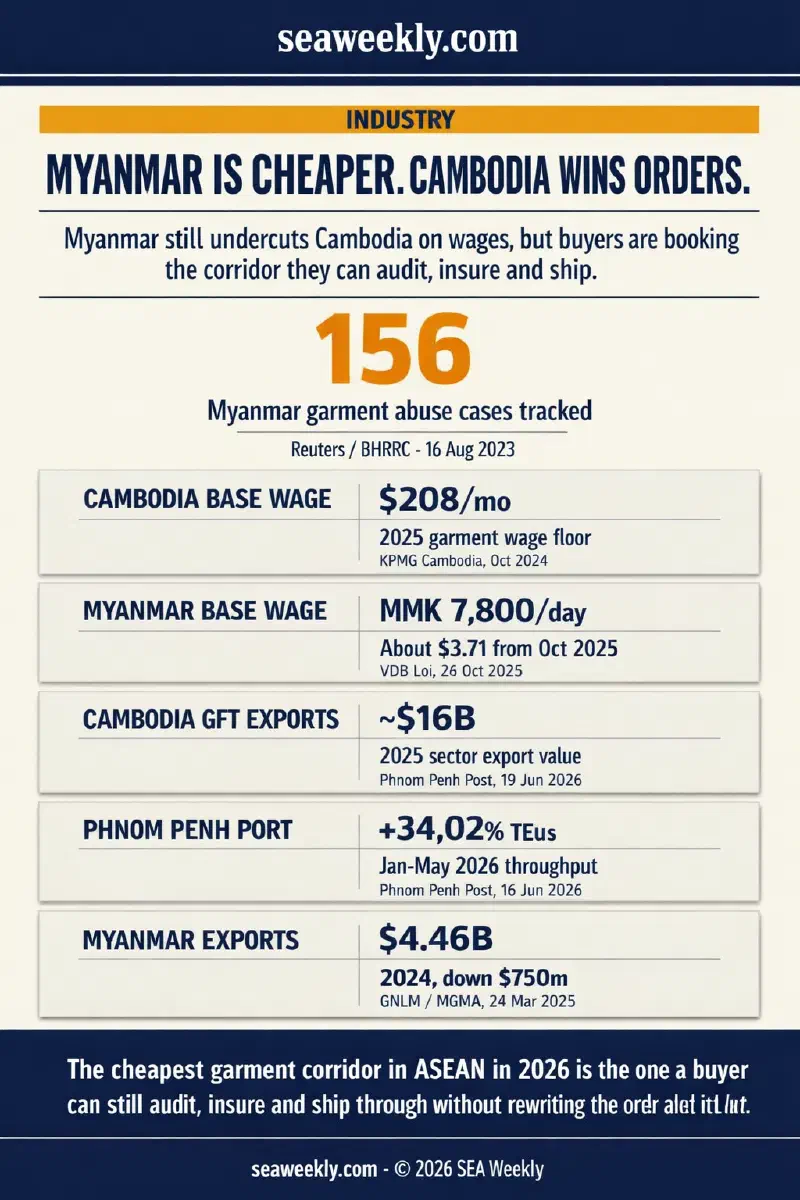

Myanmar still wins the wage spreadsheet. Cambodia is winning the orders that actually get approved.

For a sourcing manager locking autumn production in July 2026, that distinction matters more than the labour table suggests. Myanmar’s legal minimum wage is now MMK 7,800 for an eight-hour day, or about $3.71 at the exchange rate used in VDB Loi’s October 2025 legal update. Cambodia’s 2025 minimum wage for garment, textile, footwear, travel-goods and bag workers is $208 a month. On paper, Myanmar still looks like the cheaper sewing line. (VDB Loi, 24 Oct 2025) (KPMG Cambodia, Oct 2024)

But the cheapest corridor in 2026 is not the one with the lowest posted wage. It is the one a global buyer can audit, insure, finance and ship through without reopening the purchase order mid-cycle. By that standard, Cambodia is winning the mainstream low-cost garment business in ASEAN, while Myanmar is increasingly left with buyers willing to trade governance, compliance and delivery certainty for a lower labour line.

The wage sheet still says Myanmar #

This is what makes the comparison deceptively hard. If you are screening only for payroll cost, Myanmar still looks attractive. At roughly $3.71 a day, the statutory minimum wage annualizes to barely half Cambodia’s monthly garment wage floor. The Myanmar Garment Manufacturers Association is still talking like a country with runway: its 10-year plan imagines a more profitable, higher-value sector, and Global New Light of Myanmar said the industry earned $4.46 billion in export revenue in 2024, even after a roughly $750 million drop from 2023. MGMA still wants a $15 billion industry over the next decade. (Global New Light of Myanmar, 24 Mar 2025)

So the low-wage story is not fake. It is incomplete.

The mistake many buyers still make is treating wage cost as if it were the same thing as sourcing cost. It is not. Sourcing cost is wages plus every other premium that gets attached to the order after it leaves the spreadsheet: compliance monitoring, reputational exposure, payment friction, policy uncertainty, transport re-routing, insurance, and the probability that a brand’s own risk team will ask for the whole order to be reviewed again.

That is where Myanmar’s nominal advantage starts to disappear.

Why Myanmar’s discount stops being cheap #

The first problem is buyer confidence. Zara owner Inditex said in July 2023 that it was stopping purchases from Myanmar. H&M followed in August, saying it would gradually phase out sourcing from the country because it faced increasing challenges operating according to its own standards. Primark and Marks & Spencer were already on the exit path. (Reuters, 27 Jul 2023) (Reuters, 17 Aug 2023)

Those exits were not symbolic. They were a verdict on what kind of order Myanmar can still win.

Reuters reported a day before H&M’s exit decision became public that the retailer was investigating 20 alleged labour-abuse cases at Myanmar supplier factories. The same report cited a Business and Human Rights Resource Centre tracker showing 156 alleged worker-rights abuse cases from February 2022 to February 2023, up from 56 the year before. The most common allegations were wage reduction, wage theft, unfair dismissal, inhumane work rates and forced overtime. (Reuters, 16 Aug 2023)

This does not mean every order disappears. It means the buyer mix changes.

That is the part most commentary misses. Reuters also captured the counterargument from people still working on Myanmar: if the more responsible global brands leave, factories do not necessarily become cleaner or more ethical. They may simply end up chasing what Vicky Bowman called footloose buying agents who care only about cheap labour. Adidas and Next argued for staying engaged with stronger due diligence. In other words, Myanmar’s wage advantage may not vanish - it may narrow toward the buyers least likely to pay for compliance in the first place. (Reuters, 16 Aug 2023)

The second problem is policy risk. The European Union said in August 2023 that it was assessing human and labour rights in Myanmar under the enhanced-engagement framework tied to the Everything But Arms scheme. EBA still gives Myanmar tariff- and quota-free access to the EU for most goods. But once Brussels is openly saying it can adapt policy if necessary, the trade-access cushion stops looking like a permanent sourcing assumption. (Reuters, 24 Aug 2023)

The third problem is macro stability. Reporting based on World Bank analysis in June said Myanmar inflation had spiked to nearly 25% as fuel shock compounded the effects of civil war. A corridor can be cheap at the payroll line and expensive everywhere else if transport, energy and household cost pressures keep repricing the operating environment. (Free Malaysia Today, 16 Jun 2026)

Put those three together and Myanmar no longer looks like the region’s easiest low-cost garment lane. It looks like the lane that still wins only if the buyer is willing to absorb, ignore or outsource more risk.

Cambodia’s higher wage is buying something buyers can use #

Cambodia’s advantage is not that it is cheap. It is that it remains legible.

Labour Minister Heng Sour said in June that Cambodia’s garment, footwear and travel-goods sector still directly employs more than 1.2 million workers across roughly 2,000 active enterprises and supporting operations, including 1,468 garment factories. That scale matters because it gives buyers options inside a system they already understand. It also matters that Cambodia has spent years turning Better Factories Cambodia into a shorthand for auditable manufacturing rather than just low-cost assembly. (Phnom Penh Post, 17 Jun 2026)

Industry leaders are now saying the quiet part out loud. At the Cambodia Textile Summit in June, TAFTAC secretary-general Ken Loo said Cambodia could no longer rely on cost alone and that the factories most likely to succeed after LDC graduation would be the ones offering reliability, quality and a workforce able to move up the value chain. That is not a motivational line. It is a sourcing rule. (Phnom Penh Post, 19 Jun 2026)

The throughput numbers support the same story. Phnom Penh Autonomous Port handled 276,151 TEUs in January-May 2026, up 34.02% year on year, while cargo vessels rose 7.04% and cargo-plus-fuel volume rose 10.7%. A route can be expensive and still valuable if it is visible, investable and moving. (Phnom Penh Post, 16 Jun 2026)

The macro layer is hardly stress-free. The World Bank said Cambodia’s goods exports still grew 17.7% in the first quarter of 2026, while FDI reached $5.1 billion in 2025 and created an estimated 400,000 formal jobs. But the same update warned that inflation had reached 5.8% in April, growth would slow to 3.9% in 2026, and rising fuel costs were pressuring firms’ ability to sustain employment. Cambodia is not gliding through this cycle untouched. It is simply still bankable in a way Myanmar currently is not. (World Bank, 9 Jun 2026) (World Bank, 9 Jun 2026)

This is also consistent with what I argued in my June 23 Cambodia manufacturing outlook: the factories that survive H2 2026 are not the ones with the cheapest sticker cost, but the ones whose buyers can still plan around the corridor with confidence.

The 2026 verdict #

So who is winning?

If the question is who has the lower posted labour cost, Myanmar wins easily.

If the question is who is winning ASEAN’s lowest-cost garment sourcing corridor in a form that global brands can actually use, Cambodia wins.

That does not make Cambodia a clean or permanent winner. Its wage floor is higher. Its own energy and logistics costs are rising. LDC graduation will test the very trade preferences that helped build the sector. And the country’s leaders are right to worry that cost alone will no longer carry it. But Cambodia still offers what Myanmar increasingly does not: scale, auditability, buyer familiarity, and shipping visibility inside a system that can still clear a multinational risk committee.

Myanmar, by contrast, is not disappearing from the map. It is being pushed into a narrower commercial segment - buyers who still want the wage discount and are more willing to absorb labour-rights controversy, policy uncertainty and operating volatility in exchange.

That is why the 2026 answer is uncomfortable. Cambodia is not cheaper than Myanmar. Myanmar’s discount is simply being consumed by governance, compliance and delivery-risk premiums faster than Cambodia’s higher wage is eroding margins.

References:

- Reuters (27 Jul 2023). “Zara owner Inditex says it will stop buying clothes from Myanmar.” https://www.reuters.com/business/retail-consumer/zara-owner-inditex-stop-sourcing-myanmar-2023-07-27/ (Accessed 16 Jul 2026)

- Reuters (16 Aug 2023). “H&M probes alleged Myanmar factory abuses as pressure intensifies.” https://www.reuters.com/business/retail-consumer/hm-probes-myanmar-factory-abuses-pressure-intensifies-2023-08-16/ (Accessed 16 Jul 2026)

- Reuters (17 Aug 2023). “H&M says it will ‘phase out’ sourcing from Myanmar.” https://www.reuters.com/business/retail-consumer/hm-says-it-will-phase-out-sourcing-myanmar-2023-08-17/ (Accessed 16 Jul 2026)

- Reuters (24 Aug 2023). “EU monitors Myanmar labour rights as fashion brands exit.” https://www.reuters.com/sustainability/eu-monitors-myanmar-labour-rights-fashion-brands-exit-2023-08-24/ (Accessed 16 Jul 2026)

- KPMG Cambodia (Oct 2024). “TU Updates - Prakas no. 211 on the New Minimum Wage for the Textile, Garment, Footwear, Travel Goods and Bags Sectors for the Year 2025.” https://kpmg.com/kh/en/insights/2024/10/technical-update.html (Accessed 16 Jul 2026)

- VDB Loi (24 Oct 2025). “Myanmar Minimum Wage Update & Changes to Commercial Tax Exemptions for Contract Manufacturing.” https://www.vdb-loi.com/mm_publications/myanmar-minimum-wage-update-changes-to-commercial-tax-exemptions-for-contract-manufacturing/ (Accessed 16 Jul 2026)

- Global New Light of Myanmar (24 Mar 2025). “MGMA targets global markets with strategic goals for quality garments.” https://www.gnlm.com.mm/mgma-targets-global-markets-with-strategic-goals-for-quality-garments/ (Accessed 16 Jul 2026)

- Free Malaysia Today (16 Jun 2026). “Myanmar inflation hits 25% on US-Iran fuel shock, says World Bank.” https://www.freemalaysiatoday.com/category/business/2026/06/16/myanmar-inflation-hits-25-on-us-iran-fuel-shock-says-world-bank/ (Accessed 16 Jul 2026)

- Phnom Penh Post (16 Jun 2026). “Phnom Penh port sees container throughput surge by more than one-third.” https://phnompenhpost.com/business/phnom-penh-port-sees-container-throughput-surge-by-more-than-one-third/ (Accessed 16 Jul 2026)

- Phnom Penh Post (17 Jun 2026). “Sour: Garment manufacturing still engine room of Cambodian economy.” https://phnompenhpost.com/business/sour-garment-manufacturing-still-engine-room-of-cambodian-economy/ (Accessed 16 Jul 2026)

- Phnom Penh Post (19 Jun 2026). “Cambodia’s garment sector urged to move up value chain as LDC graduation nears.” https://phnompenhpost.com/business/cambodias-garment-sector-urged-to-move-up-value-chain-as-ldc-graduation-nears/ (Accessed 16 Jul 2026)

- World Bank (9 Jun 2026). “Strong Policy Action Key to Protecting Cambodia’s Jobs and Livelihoods Amid Shocks.” https://www.worldbank.org/en/news/press-release/2026/06/09/strong-policy-action-key-to-protecting-cambodia-s-jobs-and-livelihoods-amid-shocks (Accessed 16 Jul 2026)

- World Bank (9 Jun 2026). “Cambodia Economic Update, June 2026: Navigating Shocks.” https://openknowledge.worldbank.org/entities/publication/eae60100-7ec9-40cf-845a-24e93aab93f7 (Accessed 16 Jul 2026)

- SEAWeekly / P’Chai Srisuk (23 Jun 2026). “Why Cambodia Manufacturing Outlook 2026 Depends on Order-Book Quality, Not Volume.” https://seaweekly.com/posts/2026-06-23-cambodia-manufacturing-outlook-2026-order-book-quality/ (Accessed 16 Jul 2026)