The economy page tracks growth momentum, trade performance, inflation-sensitive consumer trends, and the business implications of regional demand shifts. Southeast Asia as a bloc is one of the world’s fastest-growing economic zones, with collective GDP surpassing USD 3.6 trillion and intra-regional trade deepening through RCEP and bilateral agreements. Coverage connects macro signals — GDP prints, current-account moves, currency pressure — to the ground-level commercial decisions they drive across the ten ASEAN member states.

Regional GDP: ASEAN collective output exceeds USD 3.6 trillion, ranking it among the world’s top five economic blocs

Growth leaders: Vietnam, Philippines, and Indonesia have consistently posted among the fastest GDP growth rates in the Asia-Pacific

Trade framework: The Regional Comprehensive Economic Partnership (RCEP) covers roughly 30 % of global GDP and shapes tariff exposure for every exporting nation in the region

Consumer base: A combined population of ~680 million, with a middle class projected to reach 350 million by 2030, underpins rising domestic demand

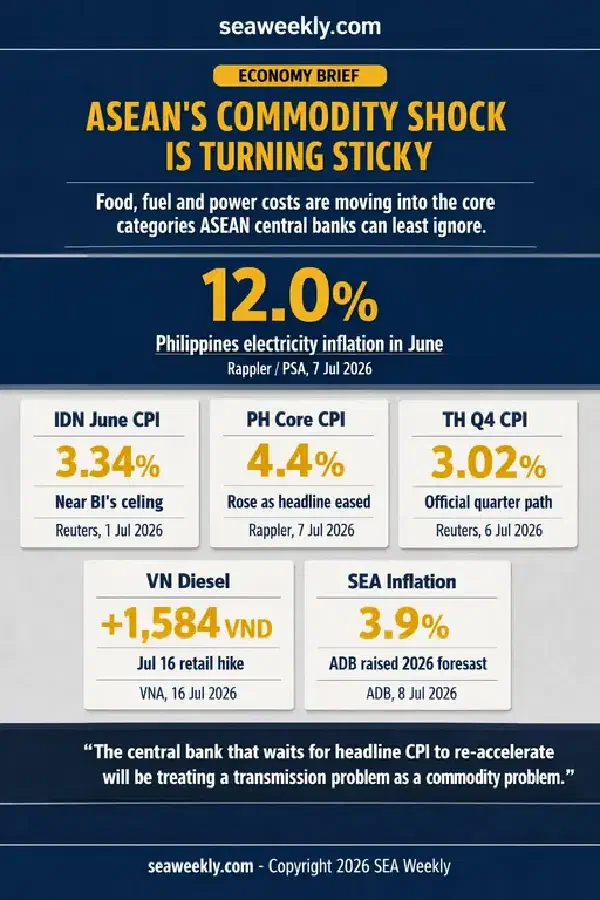

Inflation sensitivity: Food and fuel price movements carry outsized weight in household budgets, making CPI and commodity data closely watched editorial signals

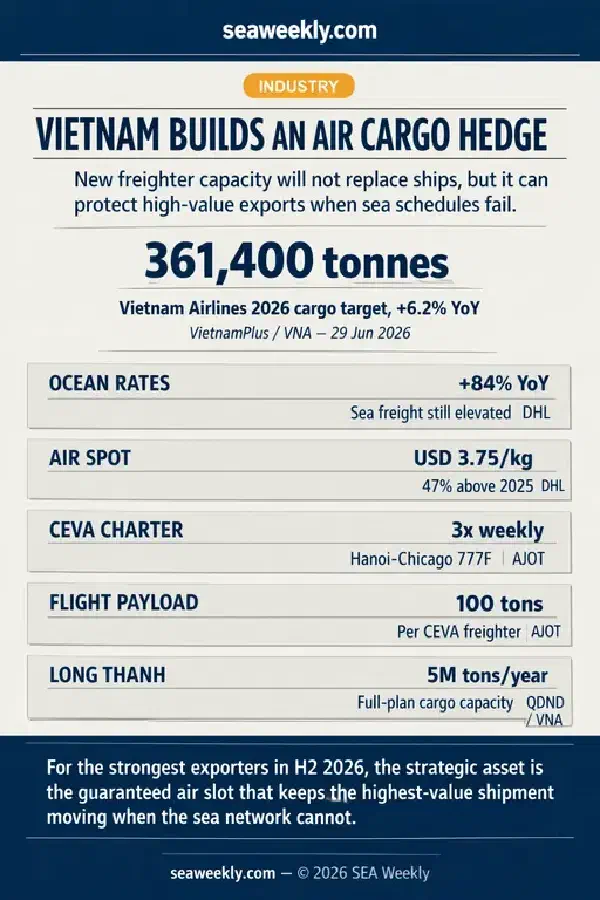

Vietnam’s air-cargo buildout is becoming a selective but strategic hedge for high-value exporters as sea-lane congestion keeps ocean schedules unreliable in H2 2026.

Vietnam’s air-cargo buildout is becoming a selective but strategic hedge for high-value exporters as sea-lane congestion keeps ocean schedules unreliable in H2 2026.

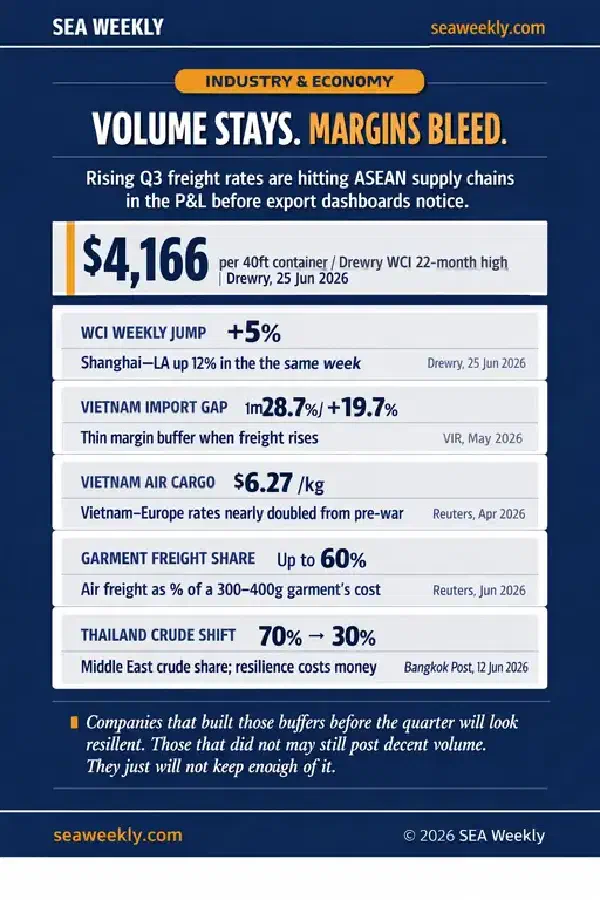

Indonesia’s June CPI data shows logistics costs already feeding consumer prices. The harder truth is that the full Q3 freight pass-through doesn’t land until Q4 — exactly when ASEAN central banks expect room to normalise.

The World Bank just upgraded the Philippines to upper-middle income status. This week’s other data — 6–7% inflation, an 11-month remittance low, and 42% digital loan delinquency rates — describes a different household reality for the families most exposed to food import inflation.

Indonesia’s June CPI data shows logistics costs already feeding consumer prices. The harder truth is that the full Q3 freight pass-through doesn’t land until Q4 — exactly when ASEAN central banks expect room to normalise.

Vietnam’s factory expansion is real. But the PMI headline at 52.8 is being carried by domestic safety-stock orders, not committed export bookings. The export order sub-index only barely turned positive in May. Until forward order depth improves, the H2 ASEAN export recovery thesis remains provisional — and Vietnam’s factory corridor is the clearest place to read that signal.

Three simultaneous repricing events are settling ASEAN’s H2 capital map. Thailand has emerged as the surprise winner — not through tourism or domestic consumption, but through AI data centre infrastructure. Indonesia’s governance premium is now a hard market fact. Singapore’s institutional moat is actively widening. The H2 growth competition was won on institutional quality, not growth rate.

Malaysia is pushing up the value ladder into semiconductor IP and advanced design while Vietnam is racing to close a localisation deficit in volume electronics manufacturing. Both strategies are legitimate. The competitive zone where they genuinely collide — advanced PCB, compound subassembly, precision electronics components — is where global supply chain investment decisions will be made and where both countries’ industrial policy ambitions are most directly tested.