The strategic asset in Vietnam’s export machine this half is not the ship. It is the guaranteed slot on a freighter.

That sounds extravagant in a country that still moves the overwhelming majority of its merchandise by sea. But H2 2026 is shaping into a logistics cycle where schedule reliability matters more than nominal freight cost for the highest-value slice of exports. When the ocean network remains technically open but operationally erratic, the fallback lane becomes strategic.

Air as insurance, not replacement #

The first thing to get clear is what this article is not arguing. Vietnam is not about to replace container ships with airplanes. It cannot. Sea freight remains the only mode that can move the country’s export scale at an acceptable unit cost.

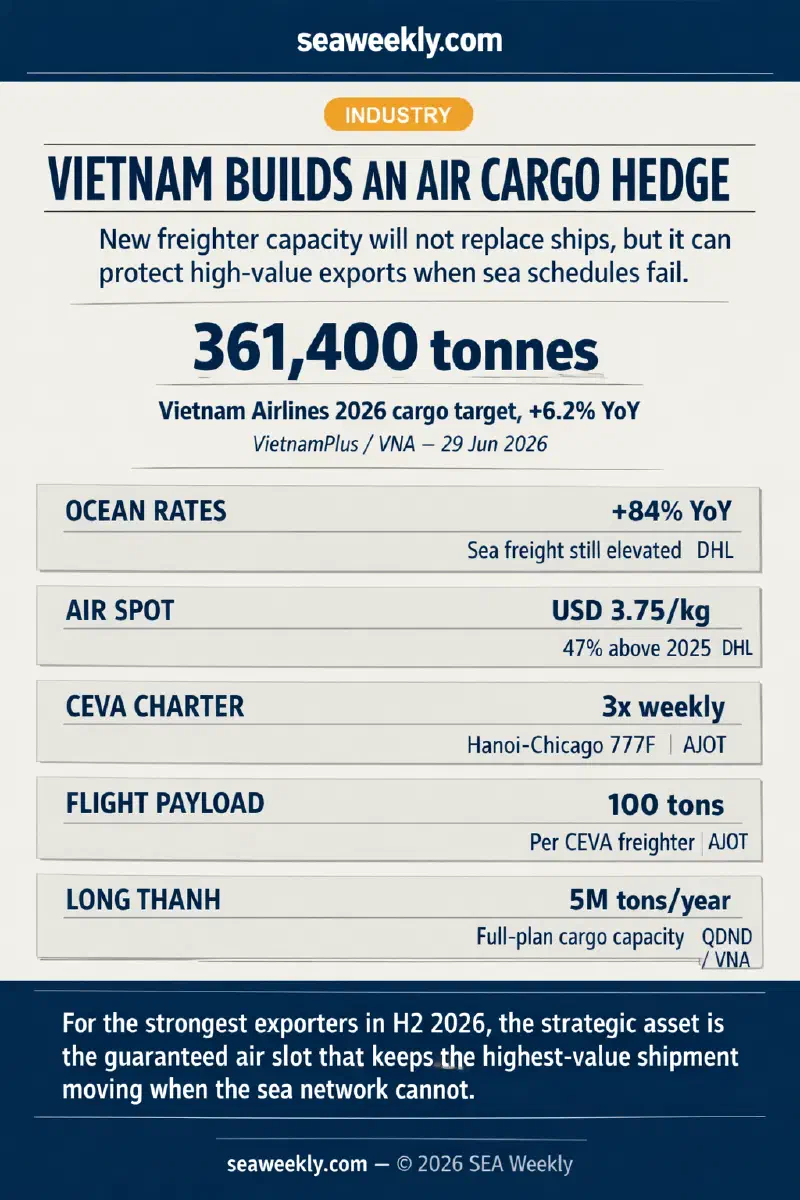

But scale is not the only variable that matters in H2 2026. Reliability matters too, and the sea side of the equation is still messy. DHL’s July ocean-freight update says effective capacity remains constrained by port congestion and ongoing Suez detours even as global fleet capacity continues to expand. Rates are still up 84 percent year on year, and westbound Far East-Europe pricing is rising again as congestion returns to levels last seen during the 2022 post-pandemic peak (DHL, July 2026). Portcast’s July 14 congestion snapshot still showed Jeddah at 4.24 days of waiting time and Sohar at 3.54 days, with long-tail delays across other ports that make published schedules look tidier than actual execution (Portcast, July 14, 2026).

That distinction matters. A sea network can be open and still be unreliable enough to break production planning. Once that happens, exporters stop asking only “what is the cheapest lane?” and start asking “which shipment absolutely cannot miss its window?”

Reuters captured this logic early in the Middle East disruption cycle. In March, it reported that more than 100 container ships had been blocked around Hormuz while airspace closures reduced freighter and passenger-belly capacity. Air freight was described by supply-chain strategists as a bridge, not a substitute: companies would move only limited quantities by air because the mode remained roughly five to ten times more expensive than ocean freight (Reuters, March 13, 2026). That is the right frame for Vietnam now. The air lane is not replacing the sea lane. It is insuring the part of the shipment that hurts most if it arrives late.

The air market is expensive, but it is functioning #

The obvious objection is that air freight is tight too. That is correct. DHL’s June air-freight update shows global air-cargo volumes up 4 percent year on year in May, with June capacity up only 3 percent. Global spot rates were still at USD3.75 per kilogram, 47 percent above last year, while Asia rates remained 30 to 50 percent above May 2025 levels (DHL, June 2026). Air Cargo Week, citing IATA data, reported global demand up 6 percent in May against only 1.9 percent capacity growth, with Asia-Pacific demand up 8 percent and the Asia-North America lane up 19.9 percent year on year (Air Cargo Week, July 2, 2026).

In other words, the hedge is not cheap. But a hedge does not have to be cheap to be rational. It has to be cheaper than the damage it prevents.

For low-margin goods, the arithmetic still fails. For semiconductors, precision electronics, urgent industrial inputs, premium garments, medical goods, or critical replacement components, the arithmetic can work very quickly. One pallet moved by air can keep a line running, hit a customer delivery date, or preserve a quarter’s worth of margin on a strategic account even if the rest of the order stays on the water.

This is exactly where Vietnam’s export structure is changing. In March, FedEx argued that Vietnam’s air-cargo growth was being pulled by the country’s move up the value chain, especially in electronics and advanced manufacturing. It cited roughly 1.3 million metric tons of cargo throughput in 2025, up 22 percent year on year, and noted that electronics accounted for more than one-third of Vietnam’s exports (FedEx, March 20, 2026). That mix is much more compatible with selective air freight than Vietnam’s earlier export model was.

The northern corridor already has usable air capacity #

The strongest evidence that this is becoming strategic rather than theoretical is that operators are committing controlled lift into Vietnam now.

On June 24, CEVA Logistics launched a Hanoi-Chicago charter program operating three times per week on Boeing 777 full freighters, with same-day departure and arrival and up to 100 tons of capacity per flight. The route was built for the sectors that matter most here: high tech, industrial, retail, and e-commerce. More important than the headline frequency is the architecture behind it. CEVA is consolidating freight across Hanoi, Danang, and Ho Chi Minh City and feeding it through the Hanoi gateway, effectively turning the north into a controlled national export node for urgent U.S.-bound cargo (AJOT, June 24, 2026).

That is the sort of operating move companies make when they believe demand is durable enough to justify dedicated capacity rather than ad hoc spot bookings. CEVA’s vice president of global air and ocean operations, Loic Gay, said the new Hanoi charter was designed to guarantee customers access to reliable and resilient capacity. The phrase to focus on is not “new route.” It is “controlled air network.” That is the language of risk management.

FedEx made a quieter but equally important move. Its additional outbound Hanoi flight, routed through Incheon and Guangzhou, gives northern Vietnam one-day faster transit times to Asia and Europe and better reliability into U.S. and Canadian destinations (FedEx Newsroom, September 25, 2025). That is a mundane operational tweak on paper. In practice, it expands the number of export managers in Bac Ninh, Thai Nguyen, Hai Phong, and Hanoi who can credibly write air optionality into their fulfilment plans.

I argued in my June 17 analysis of Vietnam’s logistics costs that Vietnam’s structural problem is not just freight rates, but the way logistics friction compounds through the inland transport and timing layers. The significance of the northern air buildout is that it gives exporters one more timing tool. It does not remove the structural cost problem. It does give managers a fallback when the most time-sensitive shipment cannot wait for the sea network to behave.

The south is building the next air layer #

The southern story is different. It is less about immediate controlled freight programs and more about airport architecture being built in real time.

ACV said on July 1 that Long Thanh International Airport is being developed across 5,000 hectares with eventual capacity of 100 million passengers and 5 million tons of cargo annually over three phases, with Phase 1 still expected to complete by the end of 2026 (QDND / VNA, July 1, 2026). The five-million-ton cargo figure is a full-buildout number, not an H2 operating number, and it should not be presented otherwise. But it still matters because infrastructure strategy starts shaping airline behavior before opening day.

ACV has already established Long Thanh air-cargo branches, is running recruitment for those units, and has scheduled three rounds of trial operations for September, October, and November. It also said Vietnam Airlines had proposed transferring around 12 percent of its international flight portfolio from Tan Son Nhat to Long Thanh under the Phase 1 operating plan (QDND / VNA, July 1, 2026). Cargo readers should not dismiss that as passenger-network housekeeping. Long-haul international flights mean belly-hold space. Belly-hold space means more options for urgent export cargo without requiring a dedicated freighter on every lane.

The physical project is also clearing milestones. VnExpress reported on June 11 that Long Thanh’s main power supply had been energized, enabling the airport’s scheduled September-November test sequence ahead of the targeted December 2026 commercial launch (MSN / eVnExpress, June 11, 2026). In last week’s corridor-upgrades piece, I argued that Long Thanh is one pillar of a broader southern logistics ring. The air-cargo version of that argument is narrower and more useful: even before the airport is fully live, it is changing how carriers and planners think about southern Vietnam’s future capacity mix.

Vietnam Airlines’ own strategy reinforces the point. On June 29, the carrier said it planned to introduce its first dedicated cargo aircraft in Q3 2026 and targeted 361,400 tonnes of cargo this year, up 6.2 percent on 2025, even while aviation fuel costs remained punishingly high (VietnamPlus / VNA, June 29, 2026). That is not a bet on cheap freight. It is a bet that reliable air capacity has become strategically necessary.

Why the hedge favors Vietnam’s newer exporters #

The part of this story that matters most for Vietnam’s medium-term development model is who benefits.

This hedge is not democratic. It does not help every exporter equally. Low-margin, bulky, ocean-dependent sectors will still live or die by vessel schedules, container pricing, and port execution. Air freight remains too expensive for that universe most of the time. The beneficiaries are the sectors with higher value density and tighter delivery tolerances: electronics, semiconductors, photonics, urgent components, and selected industrial or medical cargo.

That asymmetry is important because it aligns with the export profile Vietnam is trying to deepen anyway. In my June 30 piece on factory order visibility, I argued that Vietnam’s H2 recovery case depended less on headline PMI optimism than on whether committed orders actually turned into reliable fulfilment. Air optionality does not create those orders. It does make them easier to honour once they exist.

The best way to think about the shift is this: air freight is becoming a strategic hedge not because Vietnam has stopped being a sea-freight economy, but because its most valuable exports increasingly cannot afford to behave like one all the time.

What to watch through H2 #

Three indicators will show whether this hedge is truly becoming structural.

First, whether operators continue adding controlled capacity rather than relying on spot-market improvisation. The CEVA charter is the clearest current evidence. If more dedicated or scheduled programs appear, the thesis strengthens.

Second, whether Vietnam Airlines actually launches its first dedicated cargo aircraft in Q3 and begins building a repeatable cargo network around it, rather than treating it as a tactical experiment.

Third, whether Long Thanh’s trial sequence stays on schedule and whether route planning shifts translate into future belly-capacity expansion for long-haul markets.

The sea side of the system will still decide Vietnam’s export scale. But for the strongest exporters in H2 2026, the strategic asset is no longer only the berth, the truck slot, or the order book. It is the guaranteed air slot that keeps the highest-value shipment moving when the sea network cannot.

References #

- DHL (July 2026). “Ocean Freight Market Update.” https://www.dhl.com/th-en/home/global-forwarding/latest-news-and-webinars/ocean-freight-market-update.html (Accessed July 15, 2026)

- Portcast (July 14, 2026). “Port Congestion Snapshot: Live Vessel Wait Times (Updated Weekly).” https://www.portcast.io/blog/port-congestion-snapshot (Accessed July 15, 2026)

- Reuters (March 13, 2026). “Air freight rates soar as Middle East conflict blocks trade routes.” https://www.reuters.com/world/middle-east/air-freight-rates-soar-middle-east-conflict-blocks-trade-routes-2026-03-13/ (Accessed July 15, 2026)

- DHL (June 2026). “Air Freight Market Update.” https://www.dhl.com/vn-en/home/global-forwarding/latest-news-and-webinars/air-freight-market-update.html (Accessed July 15, 2026)

- Air Cargo Week (July 2, 2026). “Air cargo demand rises 6 percent in May despite Middle East disruption.” https://aircargoweek.com/air-cargo-demand-rises-6-percent-in-may-despite-middle-east-disruption/ (Accessed July 15, 2026)

- VietnamPlus / VNA (June 29, 2026). “Vietnam Airlines targets profit despite soaring fuel costs.” https://en.vietnamplus.vn/vietnam-airlines-targets-profit-despite-soaring-fuel-costs-post347359.vnp (Accessed July 15, 2026)

- AJOT (June 24, 2026). “CEVA boosts Asia Pacific-U.S. air cargo with two charters connecting Vietnam, China to U.S.” https://www.ajot.com/news/ceva-boosts-asia-pacific-u.s-air-cargo-with-two-charters-connecting-vietnam-china-to-u.s (Accessed July 15, 2026)

- FedEx Newsroom (September 25, 2025). “FedEx Enhances Network from Northern Vietnam to Asia and Europe.” https://newsroom.fedex.com/newsroom/asia-english/fedex-enhances-network-from-northern-vietnam-to-asia-and-europe (Accessed July 15, 2026)

- QDND / VNA (July 1, 2026). “Domestic, international airlines wish to operate at Long Thanh airport.” https://en.qdnd.vn/social-affairs/news/domestic-international-airlines-wish-to-operate-at-long-thanh-airport-592605 (Accessed July 15, 2026)

- MSN / eVnExpress (June 11, 2026). “Long Thanh, Southeast Asia’s next big airport, powers up for December opening.” https://www.msn.com/en-xl/news/other/long-thanh-southeast-asia-s-next-big-airport-powers-up-for-december-opening/ar-AA25mFUG (Accessed July 15, 2026)

- FedEx Business Insights (March 20, 2026). “Vietnam’s Air Cargo Growth: Opportunities For Exporters And Manufacturers.” https://www.fedex.com/en-sg/business-insights/tech-innovation/vietnam-air-cargo-growth-opportunities.html (Accessed July 15, 2026)

- Container News (April 17, 2026). “CMA CGM launches Gemalink Phase 2 expansion in Vietnam.” https://container-news.com/cma-cgm-launches-gemalink-phase-2-expansion-in-vietnam/ (Accessed July 15, 2026)

- SEAWeekly / Nguyen Minh An (June 17, 2026). “Why Vietnam logistics costs are still the key variable in ASEAN export recovery.” https://seaweekly.com/posts/2026-06-17-vietnam-logistics-costs-asean-export-recovery/ (Accessed July 15, 2026)

- SEAWeekly / Nguyen Minh An (June 30, 2026). “Why Vietnam factory order visibility is the key test for ASEAN export recovery in H2 2026.” https://seaweekly.com/posts/2026-06-30-vietnam-factory-order-visibility-asean-export-recovery/ (Accessed July 15, 2026)

- SEAWeekly / Nguyen Minh An (July 9, 2026). “Who is winning Vietnam’s manufacturing corridor upgrades as inter-provincial logistics demand scales up?” https://seaweekly.com/posts/2026-07-09-vietnam-manufacturing-corridor-upgrades-interprovincial-logistics/ (Accessed July 15, 2026)