The best supply chain news ASEAN frontier markets have had all year landed on Friday night — and it came wrapped in a paradox.

Pakistan’s Prime Minister posted on X that the final text of a US-Iran peace deal had been agreed, with next steps in progress (Reuters, June 12). If implemented, the agreement begins to unwind the Strait of Hormuz risk premium that has been inflating marine fuel costs, shipping insurance, and delivery overheads since February. For supply chains that connect Phnom Penh garment factories and Vientiane diesel tanks to global consumers, peace in the Gulf is the closest thing to a cost-of-goods-sold tax cut available.

But the same week produced signals that a different category of risk — governance and institutional — is now repricing upward on its own axis, and the two vectors do not cancel. They just make the risk map harder to read. That is the story that matters for anyone sourcing from, lending to, or investing in ASEAN’s frontier nodes.

The Peace Vector: What a Deal Actually Changes #

The Iran war’s supply chain footprint has been the dominant cost variable for four months. Shein and Temu’s push models stalled because jet fuel and marine freight hit levels that, as Reuters reported on June 8, “crush the margins of even the most efficient budget apparel players.” Container surcharges of $2,000-plus locked in spot-rate premiums that made Cambodia’s labor cost advantage mathematically irrelevant on a delivered-cost basis. Thailand’s refiners scrambled to adjust sourcing patterns mid-quarter (Bangkok Post, June 12).

A peace deal — even one that takes months to implement — changes the pricing forward curve immediately. Shipping insurers drop the war-risk clause. Marine fuel futures ease. Spot container rates begin normalizing toward the pre-crisis trend. For Laos, which imports roughly a quarter of its $4.4 billion in annual Thai goods as diesel, and which was only kept supplied during the March crisis because Thailand explicitly exempted it from fuel export suspensions, the arrival of cheaper energy is transformative (Laotian Times, June 3).

But here is the paradox: the peace deal lowers the cost of moving goods through the region. It does nothing for the cost of operating a business inside the region. And it is on that second ledger that this week’s data is moving in the wrong direction.

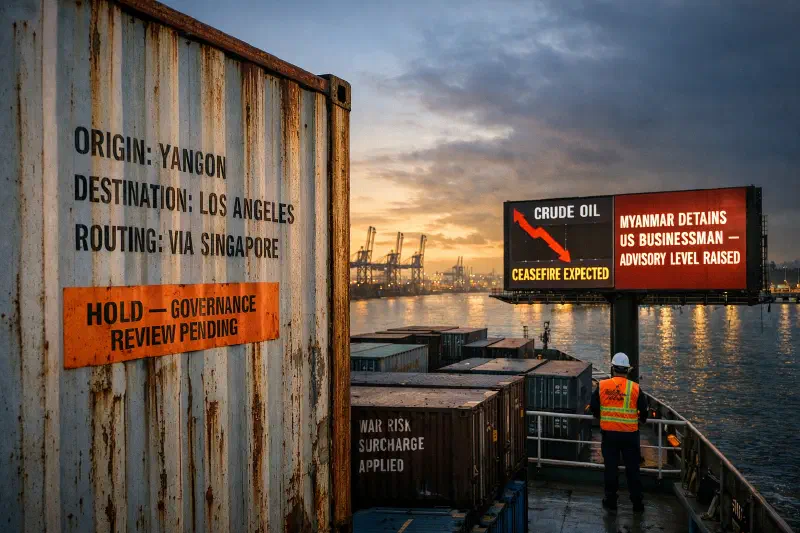

The Governance Vector: Myanmar, Indonesia, and the Institutional Drift #

On Thursday, an American businessman who wrote a book about living through Myanmar’s 2021 military coup was detained on his return to Yangon. Adam Castillo, former head of the American Chamber of Commerce in Myanmar, was stopped at the airport after a book tour abroad (Reuters, June 12). He runs a security firm in Yangon — the kind of business that exists precisely because the operating environment has deteriorated so far that personal security is now a line item on any foreign enterprise’s P&L.

This is not an isolated event. Min Aung Hlaing, the former junta chief, was sworn in as president in April following a military-engineered election that excluded all main opposition. Myanmar’s garment sector is no longer competing with Cambodia on wages because — as we argued in Tuesday’s deep dive on Cambodia-Myanmar competitiveness — the infrastructure of movement has collapsed faster than the infrastructure of making. When both the sea lanes and the roads are unreliable, cheap labor is irrelevant.

The signal from Castillo’s detention is sharper than the garment data. It says: even the Americans who stayed — who wrote books advocating more business engagement, who visited the White House to pitch rare-earth access — are no longer safe. For any multinational supply chain manager running a Myanmar exposure model, that reclassifies the country from “high-risk, insurable” to “unpriceable.” You cannot hedge against arbitrary detention.

Indonesia: A Different Kind of Governance Premium #

The governance questions in Jakarta are of a different nature, but they compound the same frontier-market problem. On Friday, students protested in the capital — some carrying signs reading “Indonesia heading for bankruptcy” — as the rupiah touched a record low of Rp 18,218 to the dollar (Reuters, June 12). Bank Indonesia has delivered 75 basis points of unscheduled rate hikes in three weeks, and the currency is still weakening.

The governance dimension is not theoretical. The revised P2SK Law, enacted June 4, expanded parliamentary oversight over Bank Indonesia, OJK, and the deposit insurance agency. Prabowo’s nephew was installed as a BI deputy governor. As we noted in last week’s analysis, the institutional framework within which credit decisions are made has shifted.

But here is where the frontier-market dimension sharpens. Danantara — Indonesia’s sovereign wealth fund — raised $1.5 billion in a debut dollar bond this week (The Business Times, June 12). Meanwhile, Pegadaian, the state-owned pawnshop and microfinance giant, quietly opened its first overseas branch in Dili, Timor-Leste in March, processing over 600 transactions and disbursing $330,000 in two months (Jakarta Post, June 10).

The contradiction is not a contradiction — it is the frontier market operating model. When domestic governance risk rises, state-linked capital looks outward. The same institutional machinery that makes foreign investors nervous about Indonesia’s rupiah is simultaneously extending credit to Timor-Leste’s micro-entrepreneurs. The risk is being exported alongside the capital.

Thailand and the Philippines: Governance Risk Edges Up #

Thailand’s consumer confidence hit a four-year low this week (Bangkok Post, June 11), while capital continued to flee Thai equities as the baht declined. The seafood trade clash with Malaysia added a cross-border friction that supply chains do not need right now (The Business Times, June 11). Neither is a governance crisis, but both are signals that domestic demand resilience — the story Malaysia has been running this quarter — is not a uniform ASEAN condition.

The Philippines’ defence chief was sanctioned by Beijing this week and responded by vowing to press on against China’s “wickedness” (Reuters, June 12). For supply chain managers, the South China Sea question is not abstract. It sits inside the same freight calculus as the Strait of Hormuz. Two maritime chokepoints, two geopolitical flashpoints — and no insurance policy that covers both simultaneously at a fixed premium.

The Adaptation Vector: Cambodia, Laos, and the Quiet Buildout #

The counter-narrative — the one that gets less attention because it is slower and less dramatic — is that some frontier markets are actively building around the risk.

Cambodia’s trade in goods passed $30 billion in the first five months of 2026, up roughly one-fifth year-on-year (Phnom Penh Post, June 10). The World Bank described the economy as resilient, citing foreign investment growth and strong exports. A South Korean manufacturing giant — KBI Group — is actively exploring Cambodian investment. Viettel Cambodia launched Metfone Express, a new logistics service, on June 9. Cross-border QR payments now reach Japan, with PPCBank among the first Cambodian banks enabled (Phnom Penh Post, June 9).

None of this makes Cambodia’s supply chain risk go away. The US DFC committed $100 million to Techo International Airport while Section 122 tariffs remain in place — a market being simultaneously taxed and funded by the same superpower. The June 9 Industrial Parks forum heard urgent calls to move past the low-cost business model before trade preferences expire. But the direction of travel is toward resilience, not away from it. That is more than can be said for Myanmar.

Laos signed its new cross-border fuel supply deal with Thailand on June 3, formalizing the dependency in a way that at least makes the volumes predictable. It is not independence. It is structured dependency. For a landlocked frontier economy with no alternative, that is the best available strategy.

The Non-Obvious Read #

The non-obvious read is this: ASEAN supply chain risk used to price on a single axis. Energy costs up? Risk up. Energy costs down? Risk down. That was the 2022-2025 model, and it worked because the Iran war was — until this week — the overwhelmingly dominant variable.

But a peace deal — even one whose text is agreed but whose implementation is pending — forces a repricing. When the energy component begins to unwind, the governance component becomes visible. And the governance component is worse than most supply chain models assume.

Myanmar is no longer priceable. Indonesia’s institutions are under scrutiny that the Danantara bond demand partially masks. Thailand’s domestic confidence is eroding while the baht weakens. The Philippines is in an active sanctions exchange with China. These are not energy stories. They do not resolve with cheaper marine fuel.

The practical implication: if you are modeling frontier-market supply chain exposure, do not expect the peace deal to deliver a proportionate reduction in your risk premium. The energy axis may give back 150 basis points. The governance axis may take 100 back. The net is still positive — but not nearly as positive as a single-variable model would predict.

Where This Arc Connects #

This argument extends four weeks of editorial arc directly.

From the June 6 SEA Weekly: Chloe Tan argued that ASEAN capital is rotating toward selective growth stories and away from undifferentiated exposure. The supply chain corollary is that risk pricing is doing the same thing. Energy risk is becoming less selective (peace benefits all). Governance risk is becoming more selective (countries diverge). The net effect is that frontier market supply chain exposure requires country-level underwriting, not ASEAN-level — exactly the same conclusion capital allocators reached about portfolio exposure.

From the June 9 garment deep dive: we introduced the concept of Logistics Entropy — the tendency of global supply chains to become more chaotic and expensive over time. This week adds the governance dimension to that framework. Logistics Entropy has a twin: Institutional Entropy. Both raise the cost of doing business in the frontier. Both are now moving independently.

From the June 9 port congestion brief: port capacity is bifurcating between new-capacity winners and aging bottlenecks. That physical bifurcation has a financial corollary: the capital that could upgrade frontier ports is the same capital that governance risk is screening out. Cambodia’s Sihanoukville port needs draught upgrades. Myanmar’s Yangon port needs everything. Neither is getting the financing it would receive if governance risk were lower.

From the June 12 Indonesia banking piece: the credit availability gap for frontier markets is widening as regional capital concentrates. This is the physical supply chain version of the same gap. When governance risk rises, both financial capital and physical infrastructure investment become scarcer for the markets that need them most.

What to Watch Next #

The single most important variable for the next two weeks is the peace deal’s implementation timeline. If a ceasefire is declared by end-June, marine fuel forward curves will move before any ship actually pays less for bunker fuel. That repricing will flow through to container rates, air freight, and cross-border trucking costs — all of which matter disproportionately for the frontier markets that have the least pricing power.

But the variable that will matter more in the medium term is governance. Myanmar is the extreme case, but Indonesia’s institutional drift, Thailand’s domestic confidence erosion, and the Philippines’ geopolitical friction are all moving in the same direction. A peace deal that lowers energy costs while governance risk continues to rise produces a net risk premium that is lower, but not low — and more complex to underwrite than the single-axis model that served through 2025.

For supply chain managers, the practical question is no longer “should I source from ASEAN frontier markets?” It is “which frontier markets have the governance trajectory to justify the logistics savings?” On that question, Cambodia and Laos are pulling ahead of Myanmar — and the gap is widening every week this war continues.

References:

- Reuters (June 12, 2026). “Pakistan PM Sharif says in X post that final text of US-Iran peace deal agreed, working on next steps.” https://www.reuters.com/world/asia-pacific/pakistan-pm-sharif-says-x-post-that-final-text-us-iran-peace-deal-agreed-working-2026-06-12/ (Accessed June 13, 2026)

- Reuters (June 8, 2026). “China’s global e-commerce push stalls as Iran war lifts costs, dampens demand.” https://www.reuters.com/business/autos-transportation/chinas-global-e-commerce-push-stalls-iran-war-lifts-costs-dampens-demand-2026-06-08/ (Accessed June 13, 2026)

- Reuters (June 12, 2026). “Myanmar detains US businessman who wrote about military coup, sources say.” https://www.reuters.com/world/asia-pacific/myanmar-detains-us-businessman-who-wrote-about-military-coup-sources-say-2026-06-12/ (Accessed June 13, 2026)

- Reuters (June 12, 2026). “Students in anti-Prabowo protests say Indonesia ‘heading’ for bankruptcy.” https://www.reuters.com/world/asia-pacific/students-hold-heading-bankrupt-indonesia-protests-against-prabowos-policies-2026-06-12/ (Accessed June 13, 2026)

- Reuters (June 12, 2026). “Philippine defence chief vows to press on against China’s ‘wickedness’ after sanctions.” https://www.reuters.com/world/china/philippine-defence-chief-vows-press-after-china-sanctions-2026-06-11/ (Accessed June 13, 2026)

- Laotian Times (June 3, 2026). “Laos, Thailand Sign New Cross-Border Fuel Supply Deal.” https://laotiantimes.com/2026/06/03/laos-thailand-sign-new-cross-border-fuel-supply-deal/ (Accessed June 13, 2026)

- Phnom Penh Post (June 10, 2026). “Cambodian Jan-May international trade up one-fifth; passes $30 billion.” https://phnompenhpost.com/business/cambodian-jan-may-international-trade-up-one-fifth-passes-30-billion/ (Accessed June 13, 2026)

- Phnom Penh Post (June 11, 2026). “Cambodia urged to move past low-cost business model as trade preference deadline looms.” https://phnompenhpost.com/business/cambodia-urged-to-move-past-low-cost-business-model-as-trade-preference-deadline-looms/ (Accessed June 13, 2026)

- Phnom Penh Post (June 9, 2026). “PPCBank Among First Cambodian Banks to Enable QR Payments in Japan.” https://phnompenhpost.com/business/ppcbank-among-first-cambodian-banks-to-enable-qr-payments-in-japan/ (Accessed June 13, 2026)

- The Business Times (June 12, 2026). “Indonesia’s Danantara unit raises US$1.5 billion as debut US dollar bond draws strong demand.” https://www.businesstimes.com.sg/international/asean/indonesias-danantara-unit-raises-us1-5-billion-debut-us-dollar-bond-draws-strong-demand (Accessed June 13, 2026)

- Jakarta Post (June 10, 2026). “Pegadaian’s first overseas venture in Timor-Leste off to strong start.” https://www.thejakartapost.com/business/2026/06/10/pegadaians-first-overseas-venture-in-timor-leste-off-to-strong-start (Accessed June 13, 2026)

- Bangkok Post (June 11, 2026). “Thai consumer confidence at 4-year low.” https://www.bangkokpost.com/business/general/3269380/thai-consumer-confidence-at-4year-low (Accessed June 13, 2026)

- Bangkok Post (June 12, 2026). “Refiners adjust sourcing as war rattles markets.” https://www.bangkokpost.com/business/general/3269625/refiners-adjust-sourcing-as-war-rattles-markets (Accessed June 13, 2026)

- The Business Times (June 11, 2026). “Thailand, Malaysia clash over seafood trade curbs.” https://www.businesstimes.com.sg/international/asean/thailand-malaysia-clash-over-seafood-trade-curbs (Accessed June 13, 2026)