ASEAN central banks are in danger of congratulating the wrong number. June headline inflation cooled in parts of the region, but the categories still accelerating - electricity in the Philippines, volatile food and packaging in Indonesia, fuel in Vietnam, and a still-rising quarterly path in Thailand - are exactly the ones that turn a commodity shock into a policy problem.

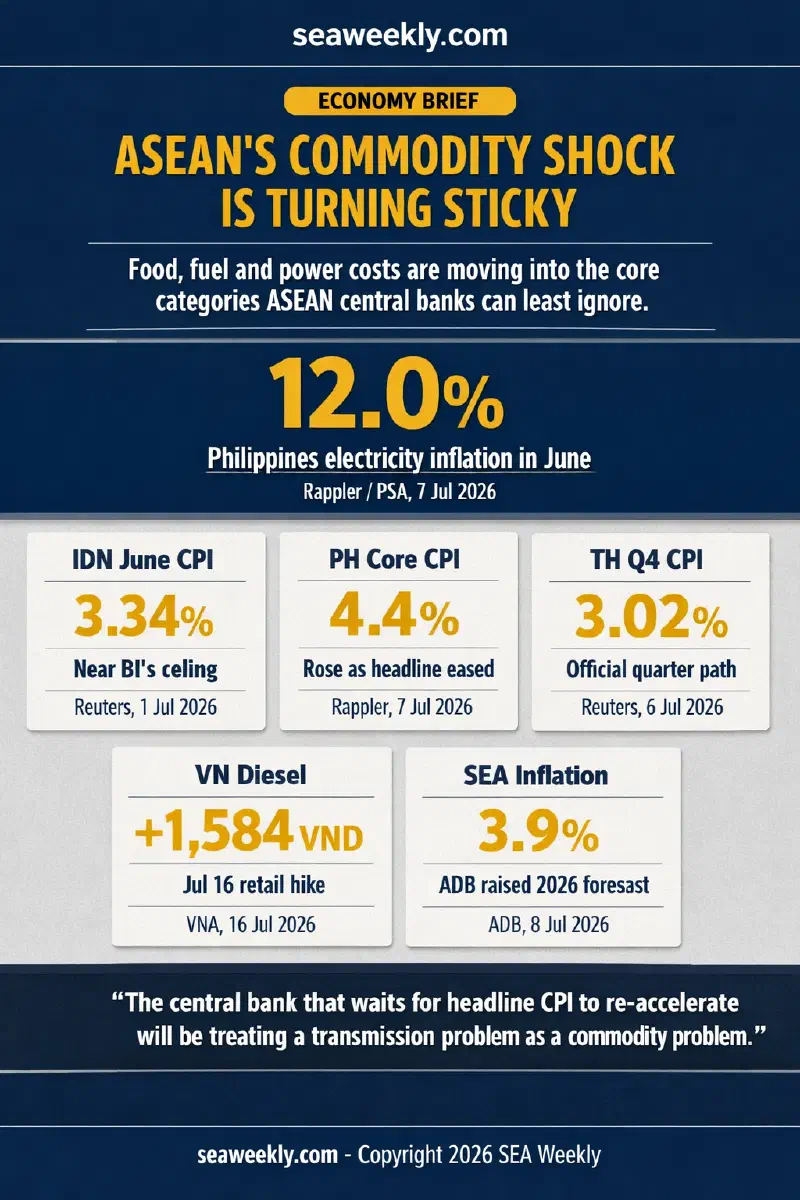

That is why commodity cost pass-through, not commodity prices alone, is the defining inflation risk for Q3 monetary policy. The Asian Development Bank has already revised its 2026 inflation forecast for developing Southeast Asia up to 3.9% from 3.2%, citing higher global energy and food prices plus exchange-rate pressure on import costs. In other words, the region is no longer dealing with a single oil headline. It is dealing with a transmission chain that is broadening as it moves downstream (ADB, July 2026; ADB, July 8, 2026).

The volatile basket is becoming the sticky basket #

The regional commodity data still tempts people into the wrong conclusion. FAO’s June release looked benign at first glance: the Food Price Index slipped 0.3% month on month to 130.3. But the components ASEAN households actually feel told a different story. The all-rice index rose 3.2% on stronger Asian demand and elevated production, transport, and marketing costs. Vegetable oils rose 3.8% month on month and 23.3% year on year. The meat index reached a new record high of 131.0 (FAO, July 3, 2026).

Oil no longer needs to spike to three-digit territory to keep the pressure alive. Brent was still at $83.62 a barrel on July 15 even as the market shrugged off renewed US attacks on Iranian military installations and focused on inventories stabilising rather than collapsing (Reuters on MSN, July 15, 2026). That is high enough to keep freight, transport, fuel, and utility bills under pressure. The more important point is that ASEAN central banks can usually look through a commodity spike. They are much less able to look through the moment when that spike starts showing up in electricity bills, restaurant menus, packaging costs, and wage-sensitive services.

As I argued in my July 2 brief on freight cost pass-through, timing matters. Q3’s newer problem is composition. The shock is no longer confined to freight and fuel. It is migrating into the slower parts of the basket.

The Philippines is already living the second round #

The Philippines is the clearest warning signal because the headline says one thing and the core basket says another. June inflation eased to 6.4% from 6.8% in May, marking the second consecutive month of deceleration after April’s 7.2% peak. That looks like progress until you read the categories underneath it.

Transport inflation was still 12.8% in June. Gasoline inflation was 39.2%, diesel 39.0%, LPG 35.0%, and electricity 12.0%. Rice inflation remained 15.0%. Restaurants, cafes, and similar establishments accelerated to 7.0%. Most important for a central bank, core inflation rose to 4.4% from 4.1% even as headline inflation eased (Rappler, July 7, 2026).

That is the pattern policymakers should worry about. The first-round commodity shock is visible in fuel. The second-round pass-through is visible in power, food service, and core categories tied to daily life rather than futures markets. The Philippine Statistics Authority explicitly flagged transport, electricity, and restaurants as risk areas going forward, while also noting the possible inflation impact of the P85 minimum wage hike in Metro Manila that takes effect in the second half of July. Meanwhile, the BSP has already raised its benchmark rate to 4.75% and left the door open to one more 25-basis-point increase.

The Philippine problem, then, is not whether inflation is falling from an uncomfortable high. It is whether the categories still rising are the ones that become self-reinforcing once they meet wages and services. That is a monetary-policy problem, not a commodity-chart problem.

Indonesia is closer to the ceiling than the headline suggests #

Indonesia’s June annual inflation accelerated to 3.34% from 3.08% in May, above the 3.20% median expectation in Reuters’ poll and uncomfortably close to Bank Indonesia’s 1.5% to 3.5% target range ceiling (Reuters on MSN, July 1, 2026). That alone would argue for caution. The more revealing signal came two weeks later, when the government made clear what it was now monitoring.

On July 14, Coordinating Minister for Economic Affairs Airlangga Hartarto said Jakarta was preparing mitigation measures not only for volatile food inflation but also for production costs that could push prices higher. Garlic was singled out. So were packaging costs. The government also linked transport-sector inflation to previously issued LPG and spare-parts import-duty waivers (Tempo English, July 14, 2026).

That matters because it shows Indonesia is no longer treating inflation pressure as a simple fuel or currency issue. The pass-through channels are widening. Food inputs, packaging materials, logistics, and transport are now part of the same policy conversation. Read that against my June 11 briefing on ASEAN fiscal-space divergence and the picture sharpens: Indonesia’s first-round shock is already colliding with the harder second-round question of how much more of the commodity bill can be buffered before it starts leaking into broader consumer categories.

Bank Indonesia does not need a fresh oil surge to face a harder Q3. It needs only a continued seepage of external costs into the items households buy every week.

Thailand and Vietnam show why soft monthly prints can mislead #

Thailand’s June CPI print looked reassuring. Headline inflation rose 2.42% year on year, down from 2.79% in May and below the 2.79% Reuters poll forecast. Core inflation was only 1.23%, still well within the central bank’s 1% to 3% target range (Reuters, July 6, 2026). On its own, that is a soft enough result to justify patience.

But the broader Thai policy picture is less relaxed than the monthly number suggests. The commerce ministry still sees headline inflation at 2.79% in Q3 and 3.02% in Q4. In April, the Bank of Thailand kept its policy rate at 1.00% but raised its 2026 inflation forecast to 2.9% from 0.3%, explicitly because of higher global energy prices, and warned inflation could exceed the target range for four quarters from the current quarter onward (Reuters / CNA, April 29, 2026). By July 12, Governor Vitai Ratanakorn was already signaling that inflation would probably come in below the bank’s earlier 2.8% forecast and that policy would remain accommodative because growth support still mattered more than a reflex rate hike (The Star / Reuters, July 12, 2026).

That is not a contradiction. It is the dilemma. Thailand is choosing to look through an external commodity shock because domestic demand is weak. The risk is not that Bangkok is ignoring inflation. It is that a softer headline print could be mistaken for the end of pass-through when policy makers themselves are still forecasting a firmer late-year path.

Vietnam offers the mirror image of the same problem. June CPI fell 0.39% month on month because fuel got cheaper. But year on year it was still up 4.69%, and first-half headline inflation averaged 4.38%. Housing, electricity, water, fuel, and construction materials rose 6.72%, transport rose 5.23%, fuel was up 8.9%, and food and catering were up 4.79% (VietnamPlus, July 3, 2026).

Then, on July 16, Vietnam raised retail fuel prices again. E5RON92 rose by 635 VND per litre, E10RON95-III by 547 VND, and diesel by 1,584 VND. Authorities used the price stabilization fund for diesel and fuel oil, while citing renewed US-Iran tensions, the Russia-Ukraine war, and Russia’s diesel export ban as the reason for higher global prices (VietnamPlus, July 16, 2026).

That is exactly what makes Q3 policy difficult. Vietnam’s monthly relief print was real, but it was also fragile. Commodity pass-through is not a straight line. It can pause for one month and restart before the celebratory commentary has even cleared.

Malaysia is the control case #

Malaysia matters in this article because it shows the region is not trapped in a single inflation script. June CPI slowed to 1.9% from 2.0% in May. Transport inflation cooled to 2.8% from 3.8%. Food and beverages held at 1.4%, while housing, water, electricity, gas, and other fuels rose 1.4% (The Star / Bernama, July 17, 2026).

That contained pass-through is why Bank Negara Malaysia has been able to keep the OPR at 2.75%, unchanged for about a year, while still describing the setting as appropriate for price stability and growth (MSN / The Rakyat Post, July 9, 2026). Malaysia is not immune to higher imported costs. It is simply showing what policy room looks like when those costs have not yet become a broad-based core inflation problem.

That is the deeper regional lesson. Commodity exposure alone does not determine the Q3 monetary-policy challenge. The decisive question is how quickly commodity costs move into the stickier parts of the basket and how much domestic policy cushioning exists before they do.

The central bank that waits for headline CPI to re-accelerate will be treating a transmission problem as a commodity problem. By the time it reacts, the shock is no longer in Brent or rice futures. It is in restaurant menus, utility bills, and wage rounds.

References #

- Asian Development Bank (July 2026). “Economic Forecasts for Asia and the Pacific: July 2026.” https://www.adb.org/outlook/editions/july-2026 (Accessed July 17, 2026)

- Asian Development Bank (July 8, 2026). “ADB Sees Slower Growth for Asia and the Pacific in 2026 Amid Global Energy Crisis.” https://www.adb.org/news/adb-sees-slower-growth-asia-and-pacific-2026-amid-global-energy-crisis (Accessed July 17, 2026)

- Reuters on MSN (July 1, 2026). “Indonesia’s June annual inflation accelerates to 3.34%.” https://www.msn.com/en-us/money/markets/indonesias-june-annual-inflation-accelerates-to-334/ar-AA26WIeV (Accessed July 17, 2026)

- Tempo English (July 14, 2026). “Indonesia Readies Inflation Control Measures.” https://en.tempo.co/read/2113709/indonesia-readies-inflation-control-measures (Accessed July 17, 2026)

- Rappler (July 7, 2026). “Inflation eases to 6.4% in June 2026 as fuel, food prices cool.” https://www.rappler.com/business/inflation-rate-philippines-june-2026/ (Accessed July 17, 2026)

- Reuters / CNA (April 29, 2026). “Thai central bank holds key rate, forecasts slower growth and higher inflation.” https://www.channelnewsasia.com/business/thai-central-bank-holds-key-rate-forecasts-slower-growth-and-higher-inflation-6088516 (Accessed July 17, 2026)

- Reuters (July 6, 2026). “Thailand’s June headline CPI up 2.42% y/y, below forecast.” https://www.reuters.com/world/asia-pacific/thai-june-headline-cpi-up-242-yy-lower-than-forecast-2026-07-06/ (Accessed July 17, 2026)

- The Star / Reuters (July 12, 2026). “Thai inflation likely below 2.8% this year, policy to remain accommodative, central bank chief says.” https://www.thestar.com.my/aseanplus/aseanplus-news/2026/07/12/thai-inflation-likely-below-28-this-year-policy-to-remain-accommodative-central-bank-chief-says (Accessed July 17, 2026)

- VietnamPlus (July 3, 2026). “Vietnam’s CPI drops 0.39% in June as cheaper fuel tempers price pressures.” https://en.vietnamplus.vn/vietnams-cpi-drops-039-in-june-as-cheaper-fuel-tempers-price-pressures-post347682.vnp (Accessed July 17, 2026)

- VietnamPlus (July 16, 2026). “Fuel prices increase in latest adjustment.” https://en.vietnamplus.vn/fuel-prices-increase-in-latest-adjustment-post348424.vnp (Accessed July 17, 2026)

- The Star / Bernama (July 17, 2026). “Malaysia’s inflation slows to 1.9% in June.” https://www.thestar.com.my/business/business-news/2026/07/17/malaysia039s-inflation-slows-to-19-in-june (Accessed July 17, 2026)

- MSN / The Rakyat Post (July 9, 2026). “Bank Negara maintains OPR, rate remained steady for a year.” https://www.msn.com/en-my/lifestyle/other/bank-negara-maintains-opr-rate-remained-steady-for-a-year/ar-AA27wQtF (Accessed July 17, 2026)

- Food and Agriculture Organization of the United Nations (July 3, 2026). “FAO Food Price Index.” https://www.fao.org/worldfoodsituation/foodpricesindex/en/ (Accessed July 17, 2026)

- Reuters on MSN (July 15, 2026). “Oil prices sink, shrugging off renewed Middle East fighting.” https://www.msn.com/en-ca/money/topstories/oil-prices-sink-shrugging-off-renewed-middle-east-fighting/ar-AA27YCTi (Accessed July 17, 2026)