The easiest mistake to make in ASEAN manufacturing right now is to wait for weaker export volumes before concluding that freight costs are doing damage. By the time the trade data rolls over, the margin hit has usually already happened inside the factory gate.

That is the more useful way to read the current Q3 shipping setup. Freight and fuel costs are rising again just as carriers regain peak-season pricing leverage, retailers frontload inventory, and exporters lock in deliveries they are reluctant to delay. The immediate consequence for Southeast Asia is not a dramatic collapse in shipments. It is a quieter and more dangerous outcome: more companies will keep volume moving while absorbing the pain through thinner gross margins.

Rates are moving higher again #

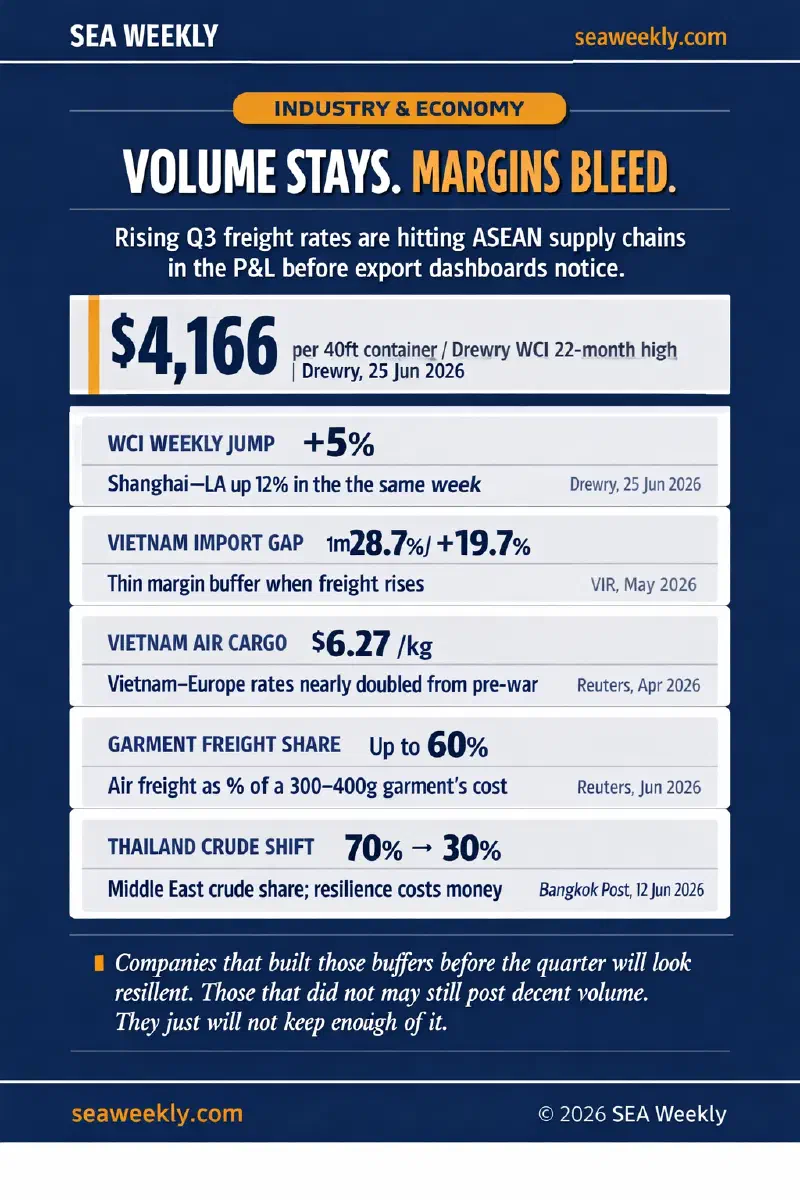

The benchmark numbers are not subtle. Drewry’s World Container Index rose 5% to $4,166 per 40ft container on June 25, its highest level since September 2024, with Shanghai-New York up 6% to $7,149 and Shanghai-Los Angeles up 12% to $5,750 (Drewry, 25 Jun 2026). More important than the level is the direction: Drewry expects additional increases in coming weeks as general rate increases, peak-season surcharges and bunker-related adjustments take effect in July.

DHL’s June ocean-freight update reaches the same conclusion from a different angle. Global demand is up 4% year to date in 2026, while fleet capacity is expected to grow only around 3%, and effective capacity remains constrained by congestion and Suez Canal detours (DHL, June 2026). That distinction matters. On paper, there are more ships. In practice, the number of reliable, well-positioned slots available to shippers is still tighter than it looks.

The geopolitical backdrop also refuses to cooperate with the optimistic version of the Q3 story. Reuters reported on June 29 that renewed US-Iran strikes again slowed energy shipping through the Strait of Hormuz, and ANZ said physical flows may take the remainder of the year to return close to pre-conflict levels (Reuters, 29 Jun 2026). That does not mean every freight lane spikes equally. It does mean the cost floor stays higher for longer than many procurement teams would prefer.

Why ASEAN feels this in margins first #

The key point is that ASEAN exporters do not experience freight inflation evenly. The burden is heaviest where local value-add is thin, imported inputs are high, and customer relationships force producers to keep shipping even when the delivered-cost math turns ugly.

Vietnam is the clearest example. The country is still in a strong manufacturing cycle: industrial production rose 9.2% year to date in the first four months, registered FDI hit $18.2 billion, and exports rose 19.7% (Vietnam Investment Review, 14 May 2026). But that same report shows imports rising even faster, up 28.7%, with production-related imports accounting for more than 94% of total imports and electronics and computer-component imports alone up 52.3% to $65.3 billion. That is a high-throughput, thin-cushion structure. When freight or bunker charges rise, there is less domestic value-add available to absorb the shock than the export headline implies.

This is why the freight story is not just about container rates. Reuters reported in April that long-term air cargo rates from Vietnam to Europe had nearly doubled to $6.27 per kilogram from pre-war levels, while companies were experimenting with awkward ship-plus-air routings via Los Angeles simply because direct options had become too expensive (Reuters, 10 Apr 2026). That is not a logistics optimization story. It is a margin-sacrifice story.

Cambodia illustrates a different version of the same logic. Trade is still growing: Jan-May international trade reached $30.08 billion, up 18.9%, with exports up 19% to $14.04 billion (Phnom Penh Post, 10 Jun 2026). On the surface, that looks resilient. But Reuters’ reporting on Chinese e-commerce exporters explains why this can be misleading for lower-value goods. Trade and Transport Group told Reuters that air freight can amount to 60% of the cost of a 300-400 gram top, while platforms like Shein are already shifting more volume into overseas warehouses to curb direct shipping costs (Reuters, 8 Jun 2026). If freight can eat that much of a simple garment’s economics, then strong shipment volume tells you very little about whether a factory is making acceptable money.

That is the uncomfortable truth many regional trade dashboards miss. Exporters often keep shipping through a freight squeeze because canceling or delaying orders risks damaging customer relationships, retailer shelf plans, and next-season allocation decisions. Revenue stays visible. Margin erosion hides underneath.

This is becoming a sorting cycle inside ASEAN #

What rising Q3 shipping rates really do is sort the region’s exporters into two camps: those that can manage logistics costs, and those that merely endure them.

Malaysia’s Penang ecosystem sits closer to the first group, though not uniformly. Penang’s manufacturing base remains one of the deepest in Southeast Asia, with more than 350 multinationals, over 6,500 manufacturing-related SMEs, and RM41.7 billion of E&E output (The Star, 26 Jun 2026). That density creates options: larger firms can consolidate cargo, negotiate contracts, regionalize inventory, or offset logistics inflation with higher-value products. But the same article also highlights why this insulation is partial, not total. The ecosystem still contains a long tail of smaller suppliers whose pricing power is weak and whose role in the value chain is too interchangeable to pass through higher freight bills cleanly.

Thailand shows another form of resilience, one that is effective but not cheap. Bangkok Post reported that imported crude accounts for 90% of Thailand’s oil consumption, and that refiners have cut the Middle East share of sourcing from nearly 70% to 30%, shifted to West Africa and the United States, and increased floating storage and reserves (Bangkok Post, 12 Jun 2026). That protects continuity. It also raises carrying costs and ties up working capital. In other words, Thailand is not escaping the freight problem. It is paying to move it from the operational column to the resilience column.

Laos is the purest pass-through case. More than 97% of its refined fuel imports come from Thailand, diesel makes up nearly a quarter of its Thai goods bill, and even during the Hormuz crisis volumes reportedly fell 25% from pre-crisis levels despite continued supply (Laotian Times, 3 Jun 2026). When freight and bunker costs rise in that system, there is barely any domestic buffer between international transport pricing and the local economy.

The broader conclusion is straightforward: the Q3 squeeze is not strongest where demand is weakest. It is strongest where logistics costs make up a high share of delivered value and where the exporter lacks the balance-sheet or commercial leverage to redesign around it.

Where this connects to the last few weeks #

This article extends several threads already visible in recent SEA Weekly coverage.

In the June 17 analysis of Vietnam logistics costs, we argued that freight volatility hits Vietnam harder because of its cost structure, not because it ships more containers than everyone else. The region-wide version of that argument is that ASEAN exporters with the least local value-add are now the most exposed even when order books remain active.

In the June 26 piece on Malaysia versus Vietnam supply-chain upgrades, the key distinction was between higher-value and lower-value layers of the electronics chain. That matters more in a freight upswing. Firms closer to design, IP, specialized components or difficult-to-replace subassemblies have a better chance of preserving pricing power. Firms living off throughput and low conversion margins do not.

And in the June 9 port-congestion brief, the argument was that physical bottlenecks were creating infrastructure winners and losers. What the current moment adds is the P&L layer: even where cargo still moves, the cost of keeping it moving is dividing strong operators from fragile ones.

What to watch in Q3 #

The first thing to watch is not export volume. It is behavior. Are manufacturers booking space earlier, holding more inventory, consolidating vendors, or shifting product mix toward higher-value shipments? Those are the signs that management teams understand the freight problem as a margin problem.

The second is whether July surcharges stick. Drewry’s expectation of further increases, combined with DHL’s view that effective capacity remains constrained, suggests carriers still have room to defend pricing into the quarter (Drewry, 25 Jun 2026; DHL, June 2026). If that happens while Hormuz traffic remains fragile, the cost squeeze will outlast the headline diplomatic cycle.

The third is where the pain shows up first in financial results. Expect it to appear not in top-line export numbers, but in weaker gross margins, higher inventory costs, and more cautious second-half guidance from companies whose supply chains depend on low-value, freight-sensitive flows.

That is the real Q3 freight story in ASEAN. Shipping rates are climbing, yes. But the more important development is that the region is entering a period where logistics discipline, pricing power and product mix matter more than raw shipment growth. Companies that built those buffers before the quarter will look resilient. Those that did not may still post decent volume. They just will not keep enough of it.

References:

- Drewry (June 25, 2026). “World Container Index - 25 Jun.” https://www.drewry.co.uk/supply-chain-advisors/supply-chain-expertise/world-container-index-assessed-by-drewry (Accessed June 29, 2026)

- DHL Global Forwarding (June 2026). “Ocean Freight Market Update.” https://www.dhl.com/th-en/home/global-forwarding/latest-news-and-webinars/ocean-freight-market-update.html (Accessed June 29, 2026)

- Reuters (June 29, 2026). “Oil climbs following renewed US, Iran strikes in Middle East.” https://www.reuters.com/business/energy/oil-climbs-following-renewed-us-iran-strikes-middle-east-2026-06-28/ (Accessed June 29, 2026)

- Reuters (April 10, 2026). “Shippers weigh unusual routes as high air cargo rates, ocean gridlock persist.” https://www.reuters.com/business/energy/shippers-weigh-unusual-routes-high-air-cargo-rates-ocean-gridlock-persist-2026-04-10/ (Accessed June 29, 2026)

- Reuters (March 13, 2026). “Air freight rates soar as Middle East conflict blocks trade routes.” https://www.reuters.com/world/middle-east/air-freight-rates-soar-middle-east-conflict-blocks-trade-routes-2026-03-13/ (Accessed June 29, 2026)

- Reuters (June 8, 2026). “China’s global e-commerce push stalls as Iran war lifts costs, dampens demand.” https://www.reuters.com/business/autos-transportation/chinas-global-e-commerce-push-stalls-iran-war-lifts-costs-dampens-demand-2026-06-08/ (Accessed June 29, 2026)

- Vietnam Investment Review (May 14, 2026). “Vietnam enters manufacturing and investment-led growth phase.” https://vir.com.vn/vietnam-enters-manufacturing-and-investment-led-growth-phase-152649.html (Accessed June 29, 2026)

- The Star (June 26, 2026). “Penang primed to prosper.” https://www.thestar.com.my/business/business-news/2026/06/26/penang-primed-to-prosper (Accessed June 29, 2026)

- Phnom Penh Post (June 10, 2026). “Cambodian Jan-May international trade up one-fifth; passes $30 billion.” https://phnompenhpost.com/business/cambodian-jan-may-international-trade-up-one-fifth-passes-30-billion/ (Accessed June 29, 2026)

- Bangkok Post (June 12, 2026). “Refiners adjust sourcing as war rattles markets.” https://www.bangkokpost.com/business/general/3269625/refiners-adjust-sourcing-as-war-rattles-markets (Accessed June 29, 2026)

- Laotian Times (June 3, 2026). “Laos, Thailand Sign New Cross-Border Fuel Supply Deal.” https://laotiantimes.com/2026/06/03/laos-thailand-sign-new-cross-border-fuel-supply-deal/ (Accessed June 29, 2026)