The most telling number in Indonesia’s nickel story this month is not US$17,000 a tonne. It is zero — the profit-sharing levy the government just scrapped. That single decision, buried in a June 10 policy pivot, captures more about who is winning Indonesia’s nickel value-capture contest than any export statistic.

The Jakarta conversation about nickel has settled into a comfortable binary. Either Chinese capital has captured the entire downstream while Indonesia watches royalties leak abroad, or President Prabowo’s downstreaming push is a triumph of industrial policy that the world should applaud. Neither story is true. And the gap between them is where the money is being made and lost in 2026.

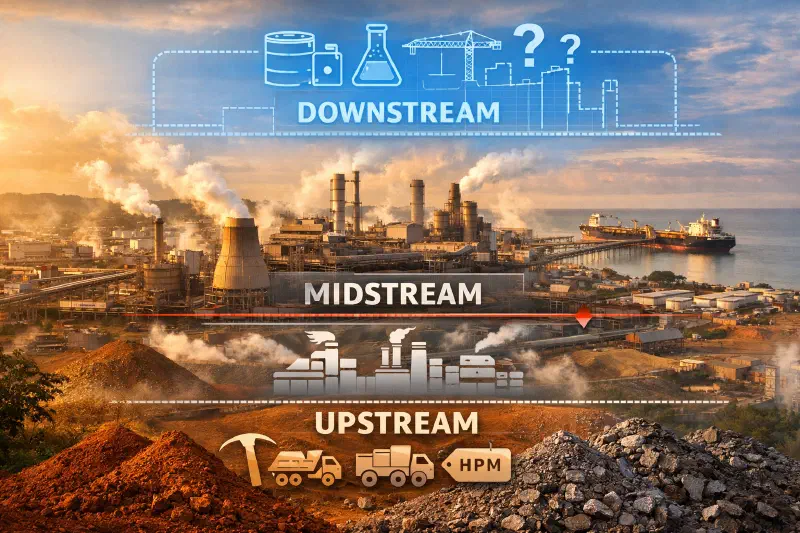

I have been tracking this sector from ports, industrial estates, and policy briefings across the archipelago for most of the year. What I see now is a value chain fragmenting into three distinct layers — upstream ore supply, midstream smelting, and downstream battery-grade processing — with a different winner at each layer. The question “who is winning?” has three different answers.

Upstream: The State Is Winning, and the Quota Relaxation Proves It #

The government’s decision to scrap the mining profit-sharing plan and relax coal and nickel quotas on June 10 was widely read as a retreat from the production discipline that Bahlil Lahadalia’s Energy Ministry signalled in late 2025 (Jakarta Post, June 10). The narrative on trading desks was straightforward: Jakarta blinked on production cuts, nickel supply will rise, and prices will soften.

That reading misses the arithmetic.

The government raised the nickel benchmark price — the Harga Patokan Mineral, or HPM — in late March, directly on President Prabowo’s instruction (Tempo English, March 26). Bahlil framed it plainly: “Our natural resources are state assets, and the President has instructed us to seek sources of income in the mineral sector that have historically not been fair to the country.” That HPM is the base against which royalties, corporate income tax, and non-tax state revenue are calculated.

Now combine the two moves: higher HPM × more ore flowing through the system = more state revenue, not less. The quota relaxation is not a surrender on price control. It is a throughput play.

The numbers support this read. Indonesia booked Rp56 trillion — roughly US$3.1 billion — in non-tax state revenue from the mineral and coal sector this year through late May (Antara, May 22). Finance Minister Purbaya Yudhi Sadewa and Energy Minister Bahlil met specifically in mid-May to find additional revenue lines from the mining sector (Antara, May 13). With the rupiah under sustained pressure, Pertamax fuel prices up 32%, and subsidy bills swelling, the government needs every revenue line it can find. Nickel is the most reliable one.

The Work Plan and Budget mechanism — RKAB — gives Jakarta an additional lever. The Energy Ministry explicitly calls RKAB “a tool to control critical minerals” (Antara, June 17). When Bahlil told Parliament on June 15 that smelter operators’ RKAB allocations are unchanged and companies should collaborate if they need more feedstock, he was not being evasive. He was telling Chinese investors the same thing in public that Prabowo told him in private: the state decides the throughput (CNBC Indonesia, June 15).

On the upstream layer, the state is winning. Not completely — illegal mining turnover estimated at Rp992 trillion is a reminder that rent-seeking leaks are still enormous (Tempo, January 30). But directionally, upstream value capture is moving toward Jakarta.

Midstream: Chinese Processors Still Dominate, but Margin Is Compressing #

Walk through the Morowali Industrial Park or the Weda Bay complex and the dominance is physical. Tsingshan, Huayou, Virtue Dragon Nickel Industry — the names on the smelter gates are overwhelmingly Chinese. This is the legacy of the 2020 nickel ore export ban: foreign processors had to build in Indonesia if they wanted access to ore, and Chinese capital was the fastest to mobilise.

The operational scale is real. Indonesia produced 2.6 million tonnes of nickel in 2025 — 66.7% of global output — and processed exports reached US$9.73 billion (Tempo, May 8). Prabowo broke ground on 13 downstream projects worth Rp116 trillion in late April, from HPAL facilities to battery material plants (Tempo, April 29). Palu Special Economic Zone secured US$1.75 billion for a battery gigafactory and LNG hub (Antara, May 13). The midstream layer is not just functioning — it is expanding.

But the friction is increasing, and Chinese operators are feeling it first.

The Chinese Chamber of Commerce formally protested royalty increases and the nickel HPM mechanism in May (CNBC Indonesia, May 13). By June, the Chinese Embassy had sent a letter to the Energy Ministry flagging policies that “could disrupt the sustainability of nickel smelter investment” (CNBC Indonesia, June 15). Bahlil’s response — we are talking, solutions are being found — was conciliatory in tone but unchanged in substance. The RKAB is not being renegotiated. The HPM is not coming down.

The margin compression for Chinese processors is structural, not cyclical. Higher HPM means higher feedstock costs. Higher royalties mean higher operating costs. Tighter RKAB control means less flexibility on volume. These are not temporary conditions. They are the new operating environment for the midstream.

This is not to say Chinese dominance is collapsing. It is not. The installed base is too large, the technical expertise too embedded, and the offtake agreements with Chinese battery makers too deep. But the era of easy margin in Indonesian nickel processing is ending. The second-generation processing investments — battery precursors, cathode active materials, recycling — will face a higher cost of capital and a more demanding government.

Downstream: The Open Race #

If the upstream is state-won and the midstream is Chinese-held but compressing, the downstream is where the genuine contest sits in mid-2026. This is Capex 2.0 — the capital-intensive, technology-heavy layer that converts nickel matte and mixed hydroxide precipitate into battery-grade material.

Three groups are positioning.

First, the Indonesian state, through Danantara. The wealth fund has taken an Australian executive to lead its resource holding company and is launching a US$1 billion global bond (Antara, May 22). Danantara wants to be the vehicle through which domestic capital — pension funds, state banks — participates in downstream nickel. The ambition is legible. The timing is difficult. As I tracked in my analysis of Indonesian banking liquidity last week, Bank Indonesia’s cumulative 75 basis points of rate hikes have pushed the 10-year government bond yield to 7.45%, raising the cost of capital for every domestic actor, including Danantara. A sovereign wealth fund issuing dollar bonds while the rupiah hits record lows is not operating from a position of financial comfort.

Second, Japanese and South Korean capital, which is building alternative supply chains. The Indonesia-Japan critical minerals and nuclear energy pact signed in Tokyo in March was explicitly about securing nickel processing pathways outside Chinese control (Tempo, March 16). Japan and South Korea have pledged roughly US$32.3 billion of investment into Indonesia, and a meaningful portion will land in battery materials. This capital is patient but demanding — it wants IRA-compliant supply chains, ESG-verifiable processing, and policy stability that the current RKAB environment does not fully provide.

Third, Western OEMs and their supply-chain partners, who face the most difficult calculus. The US has demanded Indonesia lift export restrictions on critical minerals. Indonesia has refused — the Coordinating Ministry for the Economy stated in February that the government “will not relax the ban on exporting raw commodities” (Tempo, February 23). That position is consistent with every downstreaming policy signal Prabowo has sent, but it creates a structural tension with Western buyers who want diversified ore sourcing.

The downstream layer is where the Indonesia-Philippines nickel corridor signed in Cebu on May 7 becomes relevant. Controlling 73.6% of global nickel production under a bilateral framework is not just about ore supply. It is about shaping the conditions under which battery-grade processing investment happens — and who gets to participate.

What the Mineral Exchange Tells Us #

The government’s plan to establish a new mineral and strategic commodities exchange by January 1, 2027 — mandated under the revised P2SK Law enacted on June 4 — is the institutional bet that ties all three layers together (Jakarta Post, June 17).

The ambition is clear: a domestic price discovery platform for nickel, coal, and strategic commodities that shifts benchmark-setting power away from the London Metal Exchange and Shanghai. The skepticism is equally clear. Yusuf Rendy Manilet from the Center of Reform on Economics pointed out that previous exchanges for crude palm oil (established 2023) and tin (2013) both struggled to achieve global price-setting relevance because trading volumes never reached critical mass. “A credible benchmark price can only be established if trading volumes are large, transactions are consistent, and market players trust the exchange’s mechanism,” he told the Jakarta Post. Achieving all three by January is, in his assessment, “quite ambitious.”

The exchange is the right idea at a difficult moment. It is the institutional layer that would allow Indonesia to capture value not just from ore royalties and smelter taxes, but from price discovery itself — the financialisation layer that has historically sat in London. But building liquidity, credibility, and trading infrastructure in six months, while the rupiah is under siege and Chinese smelter investors are complaining about policy predictability, is a heavy lift.

Who Is Actually Winning? #

The honest answer: different winners at different layers, and none of them cleanly.

The Indonesian state is the clearest winner at the upstream layer. Higher HPM, tighter RKAB control, the nickel corridor with the Philippines, and Rp56 trillion in non-tax mineral revenue are tangible gains. The governance risk — an Ombudsman chief arrested in a nickel corruption case, environmental damage at Pomalaa, 107 workplace deaths since 2019 — means these gains come with liabilities that are not yet on the state’s balance sheet (Tempo, April 16; Tempo, May 22). But in pure revenue terms, the state is capturing more value than at any point in the nickel cycle.

Chinese processors are winning at the midstream layer in scale terms but losing on margin. Their installed base is unchallenged. Their complaints about RKAB and royalties are a signal that the terms of engagement have shifted — from the operator-friendly environment of the 2020–2024 investment rush to a more adversarial one where the state is actively testing how much margin it can extract.

No one is winning cleanly at the downstream layer yet. Danantara has ambition but is capital-constrained. Japanese and Korean capital is committed but moving cautiously. Western OEMs want in but face the ore export ban as a structural obstacle. The downstream race is open — but it will not stay open indefinitely. The decisions made in the next twelve months about who finances and operates the precursor, cathode, and recycling plants will determine who captures the highest-value segment of the Indonesian nickel chain.

As I argued in the June 2 manufacturing comparison with Vietnam, Indonesia’s industrial advantage is not execution speed — it is scale, resource proximity, and strategic positioning. The nickel value-capture contest proves that framework. The state has the resource leverage. Chinese processors have the operational base. The downstream layer — where the real margin lives — is still being contested. The winner will be whoever brings capital, technology, and staying power into an environment where all three are becoming more expensive.

References #

- Jakarta Post (June 10, 2026). “Govt scraps mining profit-sharing plan, relaxes coal and nickel quotas.” https://www.thejakartapost.com/business/2026/06/10/govt-scraps-mining-profit-sharing-plan-relaxes-coal-and-nickel-quotas (Accessed June 18, 2026)

- Tempo English (March 26, 2026). “Indonesia to Increase Nickel Benchmark for State Revenue.” https://en.tempo.co/read/2094688/indonesia-to-increase-nickel-benchmark-for-state-revenue (Accessed June 18, 2026)

- Antara News (May 22, 2026). “Indonesia books Rp56 trillion in mineral and coal state revenue.” https://en.antaranews.com/news/416713/indonesia-books-rp56-trillion-in-mineral-and-coal-state-revenue (Accessed June 18, 2026)

- Antara News (May 13, 2026). “Finance, Energy Ministers join forces to boost non-tax state revenue.” https://en.antaranews.com/news/415661/finance-energy-ministers-join-forces-to-boost-non-tax-state-revenue (Accessed June 18, 2026)

- Antara News (June 17, 2026). “RKAB as tool to control critical minerals: ESDM Ministry.” https://en.antaranews.com/news/419403/rkab-as-tool-to-control-critical-minerals-esdm-ministry (Accessed June 18, 2026)

- CNBC Indonesia (June 15, 2026). “Investor Smelter Nikel China Keluhkan RKAB Tambang, Ini Jawaban Bahlil.” https://www.cnbcindonesia.com/news/20260615190330-4-743055/investor-smelter-nikel-china-keluhkan-rkab-tambang-ini-jawaban-bahlil (Accessed June 18, 2026)

- Tempo English (May 8, 2026). “Indonesia Launches Nickel Corridor Deal with Philippines.” https://en.tempo.co/read/2102600/indonesia-launches-nickel-corridor-deal-with-philippines (Accessed June 18, 2026)

- Tempo English (April 29, 2026). “Prabowo Breaks Ground on 13 Downstream Projects Worth Rp116 Trillion.” https://en.tempo.co/read/2100973/prabowo-breaks-ground-on-13-downstream-projects-worth-rp116-trillion (Accessed June 18, 2026)

- Antara News (May 13, 2026). “Palu SEZ secures US$1.75 billion for battery gigafactory and LNG hub.” https://en.antaranews.com/news/415624/palu-sez-secures-us175-billion-for-battery-gigafactory-and-lng-hub (Accessed June 18, 2026)

- Jakarta Post (June 17, 2026). “Liquidity, credibility risks cloud mineral exchange plan.” https://www.thejakartapost.com/business/2026/06/17/liquidity-credibility-risks-cloud-mineral-exchange-plan (Accessed June 18, 2026)

- Tempo English (April 16, 2026). “Indonesia’s Ombudsman Chief Named Suspect in Nickel Corruption Case.” https://en.tempo.co/read/2098609/indonesias-ombudsman-chief-named-suspect-in-nickel-corruption-case (Accessed June 18, 2026)

- Tempo English (May 22, 2026). “The Nickel Curse Strikes Pomalaa.” https://en.tempo.co/read/2104868/the-nickel-curse-strikes-pomalaa (Accessed June 18, 2026)