Industry coverage focuses on factories, industrial estates, energy systems, trade logistics, and the operational backbone of Southeast Asia’s growth story. The region is in the middle of a generational supply-chain reshaping: electronics and semiconductor investment is surging into Malaysia, Vietnam, and Thailand, while Indonesia’s nickel-to-EV battery corridor and Laos’s rail-linked logistics are redefining what “made in Southeast Asia” means. Energy transition stories — solar capacity, LNG infrastructure, and hydropower export contracts — run alongside the factory-floor narratives that define the region’s industrial identity.

Manufacturing shift: Tariff pressures and China-plus-one strategies are accelerating factory relocation into Vietnam, Thailand, Malaysia, and Indonesia, with semiconductor fabs leading the investment wave

Energy mix: The region blends hydropower (Laos, Vietnam), geothermal (Philippines, Indonesia), LNG (Brunei, Malaysia), and rapidly scaling solar capacity across multiple markets

Industrial estates: Hundreds of designated industrial parks and special economic zones across ASEAN compete for FDI with differentiated incentive packages and logistics connectivity

Port infrastructure: Singapore, Port Klang, and Tanjung Priok (Jakarta) are among Asia’s busiest container ports; inland connectivity via road, rail, and river is a persistent bottleneck story

EV supply chain: Indonesia’s nickel reserves and battery-processing ambitions position it as a critical node in the global electric-vehicle supply chain

Malaysia is pushing up the value ladder into semiconductor IP and advanced design while Vietnam is racing to close a localisation deficit in volume electronics manufacturing. Both strategies are legitimate. The competitive zone where they genuinely collide — advanced PCB, compound subassembly, precision electronics components — is where global supply chain investment decisions will be made and where both countries’ industrial policy ambitions are most directly tested.

Cambodia’s manufacturing volume headlines look strong, but the factories that survive H2 are those with BFC-audited buyers and non-commodity order books — not those that frontloaded before tariff uncertainty resolved.

Indonesia’s nickel value capture in 2026 is not a single story of triumph or capture — it is a three-layer contest between the state, Chinese processors, and new entrants, and each layer has a different winner.

Vietnam’s export recovery is real, but logistics costs at 16–20% of GDP mean every freight-rate swing hits exporters harder here than anywhere else in ASEAN — and the US-Iran peace deal won’t deliver a clean cost reset.

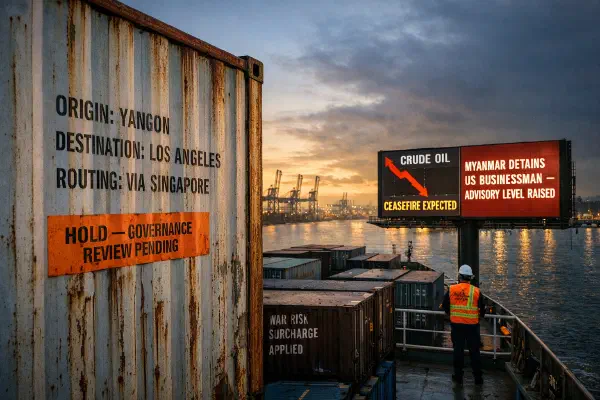

The US-Iran peace deal is the best supply chain news ASEAN frontier markets have had all year. But governance risk is now repricing upward on its own axis, and the net premium may not fall as much as logistics alone would suggest.

Brunei is taking the right institutional steps toward post-hydrocarbon diversification, but the pieces aren’t yet connected, the sovereign wealth lever remains under-deployed, and the Iran war windfall is both the best enabler and the biggest trap.

Southeast Asia’s garment sector is facing a reckoning where the savings of low-cost manufacturing are being erased by “Logistics Entropy”—the combined cost of surging fuel, worker safety crises, and unpredictable US trade policy. Cambodia is repositioning as a “stable but expensive” hub, while Myanmar is increasingly viewed as a “no-go” zone for all but the most risk-tolerant.

The key ASEAN shift this week is not whether money is coming in, but where it is willing to stay. Investors are concentrating on execution-dense, policy-credible growth nodes and treating the rest of the region as higher-carry exposure.

Vietnam’s electronics and industrial-input exports are recovering strongly, supported by FDI scale, better order flow, and ecosystem depth. But this is not yet a full value-capture recovery. Input imports are rising almost as quickly as exports, shipping costs have surged again, and origin-traceability pressure is increasing under US tariff scrutiny. The decisive question for H2 2026 is no longer whether exports rebound — it is whether Vietnam can protect margins and deepen local supplier capability before the next global shock.

The manufacturing contest between Indonesia and Vietnam is no longer about picking one winner. Vietnam remains the faster export platform; Indonesia is gaining importance as a hedge for tariffs, resources, and upstream scale. The smarter ASEAN supply-chain strategy now assigns each country a different role.