Industry coverage focuses on factories, industrial estates, energy systems, trade logistics, and the operational backbone of Southeast Asia’s growth story. The region is in the middle of a generational supply-chain reshaping: electronics and semiconductor investment is surging into Malaysia, Vietnam, and Thailand, while Indonesia’s nickel-to-EV battery corridor and Laos’s rail-linked logistics are redefining what “made in Southeast Asia” means. Energy transition stories — solar capacity, LNG infrastructure, and hydropower export contracts — run alongside the factory-floor narratives that define the region’s industrial identity.

Manufacturing shift: Tariff pressures and China-plus-one strategies are accelerating factory relocation into Vietnam, Thailand, Malaysia, and Indonesia, with semiconductor fabs leading the investment wave

Energy mix: The region blends hydropower (Laos, Vietnam), geothermal (Philippines, Indonesia), LNG (Brunei, Malaysia), and rapidly scaling solar capacity across multiple markets

Industrial estates: Hundreds of designated industrial parks and special economic zones across ASEAN compete for FDI with differentiated incentive packages and logistics connectivity

Port infrastructure: Singapore, Port Klang, and Tanjung Priok (Jakarta) are among Asia’s busiest container ports; inland connectivity via road, rail, and river is a persistent bottleneck story

EV supply chain: Indonesia’s nickel reserves and battery-processing ambitions position it as a critical node in the global electric-vehicle supply chain

Indonesia and the Philippines are squeezing ASEAN’s vessel pool from opposite sides of the commodity chain in Q3 — and neither alone would do it, but together, in monsoon season, they are.

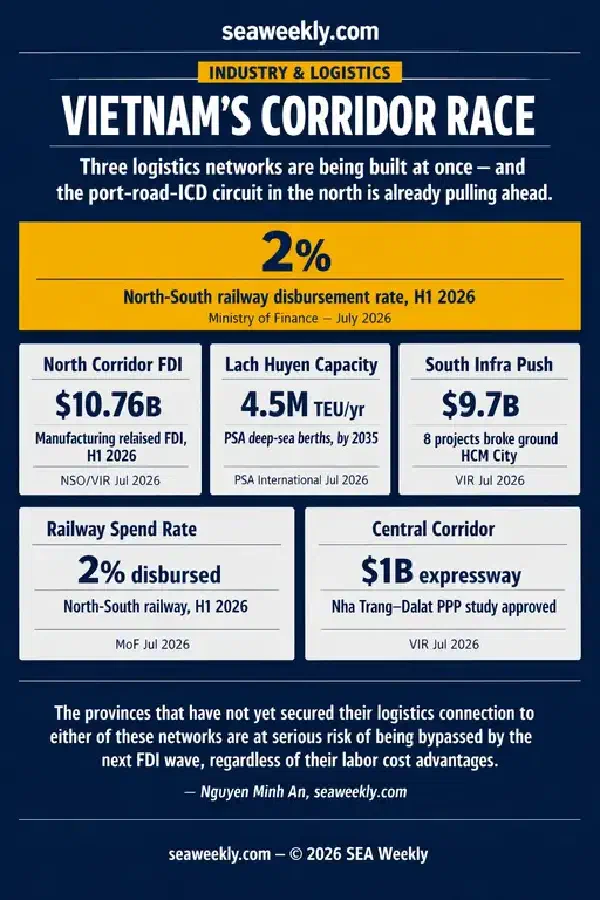

Vietnam’s manufacturing corridor race is not being won by the provinces with the most FDI — it is being won by the ones building multimodal logistics bridges to deep-water ports before capacity tightens.

Vietnam’s manufacturing corridor race is not being won by the provinces with the most FDI — it is being won by the ones building multimodal logistics bridges to deep-water ports before capacity tightens.

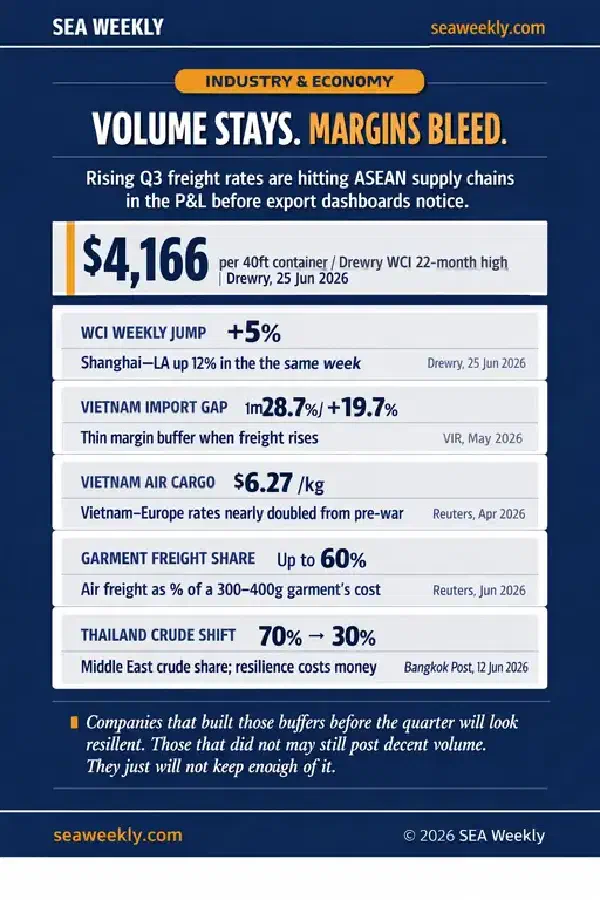

As Q3 freight rates hit 22-month highs, Malaysia’s multi-modal logistics infrastructure and lower cost burden per export dollar are re-rating the country’s electronics supply chain proposition — but the advantage belongs more to its multinational tier than to the SME supplier base.

As Q3 freight rates hit 22-month highs, Malaysia’s multi-modal logistics infrastructure and lower cost burden per export dollar are re-rating the country’s electronics supply chain proposition — but the advantage belongs more to its multinational tier than to the SME supplier base.

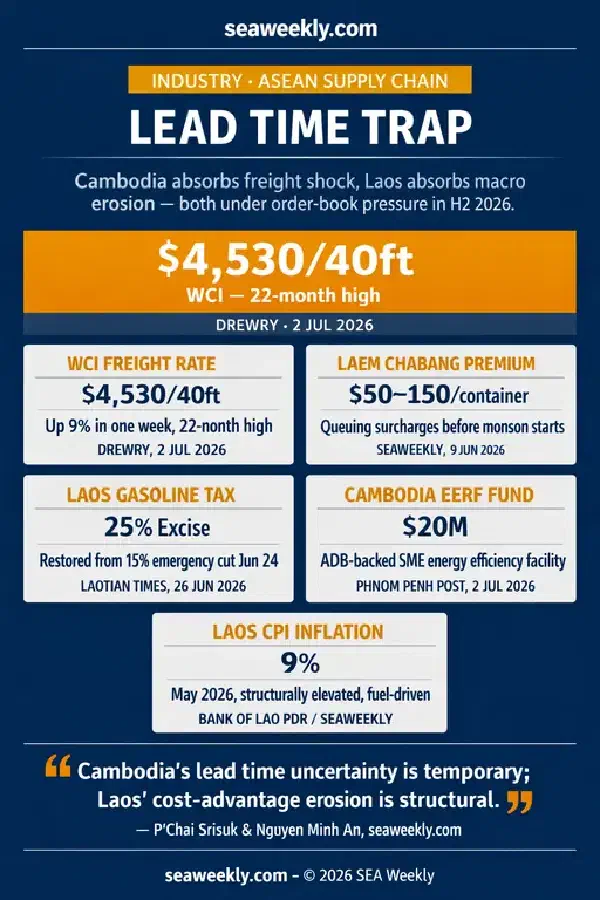

Cambodia and Laos are both under garment export pressure in H2 2026, but from opposite directions — and the window for H2 order booking is open right now.

Cambodia and Laos are both under garment export pressure in H2 2026, but from opposite directions — and the window for H2 order booking is open right now.

The three cost pressures squeezing Indonesia’s nickel downstream in H2 — freight inflation, government policy risk, and monsoon-season geography — are not hitting in sequence. They’re hitting simultaneously.

Thailand’s Laem Chabang meets its most dangerous Q3 window in years: queuing premiums already running before the first monsoon squall, rates at 22-month highs, and a manufacturing sector in contraction heading into peak disruption season.

Vietnam’s factory expansion is real. But the PMI headline at 52.8 is being carried by domestic safety-stock orders, not committed export bookings. The export order sub-index only barely turned positive in May. Until forward order depth improves, the H2 ASEAN export recovery thesis remains provisional — and Vietnam’s factory corridor is the clearest place to read that signal.