Thailand is Southeast Asia’s second largest economy, with a population of around 70 million and a highly diversified industrial base anchored by automotive manufacturing, food processing, and electronics. The country is consistently the most visited in the region, with Bangkok ranking among Asia’s top city destinations and coastal resorts in Phuket, Koh Samui, and Krabi sustaining a premium hospitality sector. Consumer credit, retail banking, and tourism-linked financial services drive domestic finance stories, while Muay Thai, football, and Formula E motorsport generate significant commercial and media value.

Commercial operators are retreating from ASEAN sports rights. Telecoms and state broadcasters are filling the gap. The structural repricing of sports sponsorship is now underway — and it will reshape who sponsors ASEAN sport, at what price, and through what channel.

Thailand is actively raising prices across airlines and hotels and demand holds. The Philippines’ high per-visitor yield is a supply constraint, not a strategy — and the distinction is the most important signal in ASEAN tourism right now.

This week’s ASEAN signal is not about growth; it is about systems integration — the markets where fintech infrastructure and industrial throughput are closing into a single investable stack are attracting better capital, on better terms, than those where the two layers are still moving on separate calendars.

Philippine aviation demand is surging but infrastructure constraints and visa barriers mean the benefits are increasingly captured by ASEAN competitors with better capacity to serve high-yield travellers.

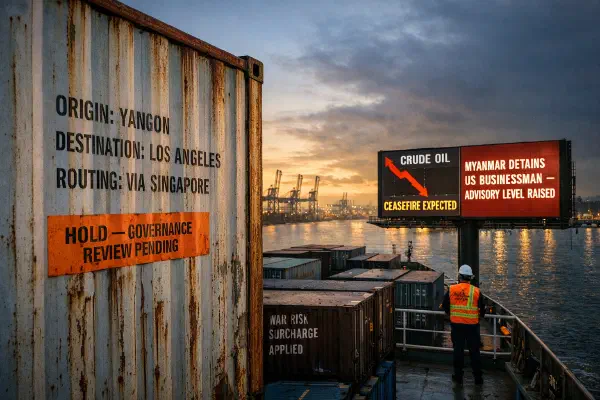

Vietnam’s export recovery is real, but logistics costs at 16–20% of GDP mean every freight-rate swing hits exporters harder here than anywhere else in ASEAN — and the US-Iran peace deal won’t deliver a clean cost reset.

ASEAN loan growth numbers are hiding a deeper liquidity stress in the deposit base — and when liquidity tightens, loan growth is the last metric to turn.

Singapore’s institutional premium model and Malaysia’s consumer ecosystem model represent two fundamentally different answers to the same question — how to turn digital payments ubiquity into profit — and the gap between them is reshaping fintech strategy across ASEAN.

The US-Iran peace deal is the best supply chain news ASEAN frontier markets have had all year. But governance risk is now repricing upward on its own axis, and the net premium may not fall as much as logistics alone would suggest.

ASEAN’s fiscal divergence in 2026 is not primarily about who exports oil. It’s about who made subsidy reform calls in the quiet years before the shock — and Malaysia and the Philippines are holding more fiscal cards going into H2 than Indonesia or Thailand.

Laos inflation is running at 9% because the country is structurally pinned: it produces 83% of its energy from hydropower yet cannot keep Électricité du Laos solvent, and it has zero domestic refining capacity yet imports 97% of its fuel from Thailand.

The key ASEAN shift this week is not whether money is coming in, but where it is willing to stay. Investors are concentrating on execution-dense, policy-credible growth nodes and treating the rest of the region as higher-carry exposure.