Right now, sourcing managers at H&M, Inditex, and PVH are running the numbers on Q4 replenishment. The window for locking in H2 garment production commitments — the orders that fill October and November shelves — closes in the next three to four weeks. What those numbers reveal, if you’re honest about the freight reality and the operational risks, is that the traditional Cambodia vs. Laos comparison no longer runs in the direction most buyers assume.

Cambodia is facing a cost-stack crisis it cannot resolve before the booking deadline. Laos is sitting on a structural advantage — the China-Laos railway — that buyers routinely misread. Understanding the difference between the two is the most consequential sourcing decision managers in the EU and US face this month.

Cambodia’s freight exposure is running hot before the season starts #

Cambodia’s garment and footwear sector is the country’s single largest export earner, employing more than 700,000 workers and generating approximately $9 billion annually. Its principal export route runs from factory floor in Phnom Penh’s industrial estates to Preah Sihanouk Port, then onto feeder vessels connecting to the deep-sea transhipment hubs at Laem Chabang in Thailand and PSA terminals in Singapore.

That two-step routing is now running into back-to-back headwinds.

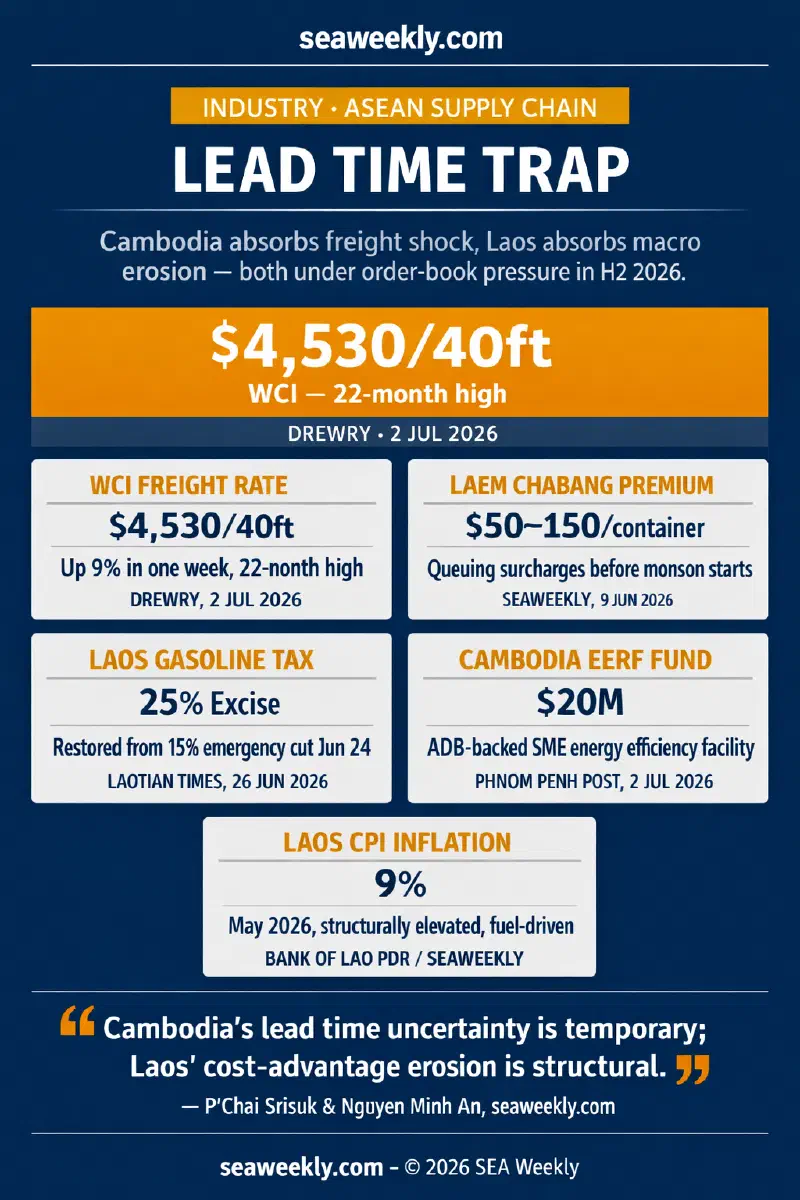

Drewry’s World Container Index stood at $4,530 per 40ft container on July 2 — up 9% in a single week and at a 22-month high. Shanghai-to-Los Angeles had risen to $5,750 (+12% week-on-week) and Shanghai-to-New York to $7,149 (+6%). Maersk, the world’s second-largest container carrier, captured the trajectory from the other side when it lifted its full-year EBITDA guidance this week to $8-10 billion from $4.5-7 billion, explicitly citing sustained spot rate increases as the primary driver. (FreightWaves, 30 Jun 2026)

For a Cambodian garment factory quoting an October delivery order at today’s spot rates, freight costs have risen approximately 35-40% against late-2024 baselines. On a $200 FOB shirt, the additional landed freight burden is $15-20 per unit when absorbed at spot. That is not a margin the buyer absorbs silently — it becomes a renegotiation pressure or a cancelled order.

The port routing problem compounds this. Laem Chabang — Cambodia’s primary deep-sea gateway — is entering the Q3 monsoon window with berth queuing premiums of $50-150 per container already running before the first significant storm system. As I documented in SEAWeekly’s July 1 analysis of Thailand’s port congestion cycle, Laem Chabang handles roughly 70% of Thailand’s total container throughput and is operating at near-maximum design capacity. The Thai Meteorological Department’s monsoon advisory was active as of June 30, warning of 2-3 metre waves in the Gulf of Thailand and upper Andaman corridors that feed the port’s vessel scheduling. (The Nation Thailand, 30 Jun 2026)

Garment spot orders from Cambodia to EU buyers had lead times of approximately 35-42 days under normal conditions. Under Q3 2026 conditions, that range expands to 40-55 days with meaningful uncertainty at either end. The variance is as damaging as the extension — buyers managing tight Q4 restocking schedules cannot build inventory plans on a 15-day uncertainty band.

There are genuine structural responses underway. The $20 million ADB-backed Energy Efficiency Revolving Fund, launched July 2, targets Cambodian SMEs including garment factories for concessional lending to replace inefficient equipment — with energy costs representing 8-12% of operating costs, the potential savings are real. (Phnom Penh Post, 2 Jul 2026) A June 30 consultation on amended customs legislation is designed to reduce clearance friction. (Phnom Penh Post, 30 Jun 2026) These are correct interventions. They accrue over 12-24 months; the H2 booking window closes in weeks.

A final wrinkle that wasn’t in the picture a month ago: the July 5 border incident at Oddar Meanchey province, where four Cambodian soldiers were injured and Thailand denied involvement, introduced a level of political tension at the border crossing Cambodia’s land-route logistics depend on. (Phnom Penh Post, 6 Jul 2026) Minor militarily. Unwelcome when lead times are already volatile.

Laos: a structural advantage being eroded from below #

Against that backdrop, Laos should be capturing order books that Cambodia is losing. The case looks compelling: a headline monthly minimum wage of approximately $130 versus Cambodia’s $204 in 2026, EU EBA (Everything But Arms) zero-duty status for European exports, and the China-Laos railway cutting Chinese fabric resupply from three-plus weeks by sea to approximately three days by rail from Kunming to the Saysettha Development Zone on the outskirts of Vientiane.

The macro environment surrounding those advantages in July 2026 is actively compressing them.

On June 24, Laos restored fuel excise taxes cut in March as emergency measures against surging oil prices. Regular gasoline excise returned from 15% to 25%; diesel jumped from zero to 5%. Retail fuel prices in Vientiane adjusted immediately: regular gasoline at LAK 30,690 ($1.38 per litre), diesel at LAK 24,560 ($1.11), premium at LAK 35,840 ($1.62). (Laotian Times, 26 Jun 2026) For garment factories running production lines, diesel backup generators, and truck-based inland export logistics, that is a direct input cost increase landing in the middle of the H2 order-booking window.

The power supply context makes the fuel point worse. Électricité du Laos ran scheduled power cuts across four Vientiane Capital districts from July 1-5, a visible symptom of the state utility’s ongoing fiscal stress. As Nguyen Minh An documented in his June 10 SEAWeekly analysis of Laos’ structural energy crisis, EDL’s debt burden is a key contributor to Laos’ public debt, complicated by opaque power purchase agreements and absence of cost-reflective tariffs. A factory in Saysettha SEZ that cannot guarantee 12-hour uninterrupted production runs cannot make the delivery reliability commitments a committed H2 buyer requires.

Laos CPI was running at 9% in May 2026 — structurally elevated and input-driven. The kip’s ongoing depreciation adds a further squeeze: fabric imported from China via the railway may be priced in yuan, but informal labour markets have increasingly dollar-referenced wage expectations, compressing the factory-level margin that was supposed to be the foundation of the Laos cost advantage. The World Bank’s July 1 income classification confirmed that Laos, alongside Cambodia and Myanmar, remains in the lower-middle-income category — a structural signal that the economy hasn’t built the institutional buffers to absorb compound shocks. (Laotian Times, 4 Jul 2026)

Minh An’s take: the railway advantage is real but misread #

The China-Laos railway changes Laos’ supply chain DNA at the input end — and nowhere else. A garment factory in Saysettha SEZ can genuinely work with Chinese fabric mills in Zhejiang on a 72-hour replenishment cycle rather than waiting three weeks for a sea shipment. That speed-of-response advantage is real, durable, and meaningful for factories with strong Chinese supplier relationships.

But once those garments are assembled, they still leave Laos by truck. Via Thailand: Vientiane or Savannakhet to Mukdahan, across the Mekong, through Nakhon Ratchasima, to Bangkok, to Laem Chabang — where you arrive at exactly the same berth queuing premiums and monsoon congestion as Cambodia’s containers. Via Vietnam: Lao Bao or Dan Tia border, overland to Da Nang or Hai Phong — where you add 2-4 days transit and at least one additional customs handoff against direct Preah Sihanouk Port access.

The buyers looking at Laos’ railway story are reading a resupply advantage as a delivery advantage. It isn’t. The freight problem doesn’t start at the Yunnan border; it starts at the export-facing port. And Laos doesn’t have one.

The order-book quality split #

These lead time dynamics map to a more fundamental divergence in order-book quality — and quality matters more than volume in an H2 planning period under stress.

Cambodia has been a major garment exporter since the mid-1990s. The Garment Manufacturers Association in Cambodia (GMAC) operates compliance frameworks, labour standards auditing, and buyer relations infrastructure built over three decades. When H&M or Levi’s places a committed H2 order in Cambodia, it sits inside a long-standing vendor relationship with established quality monitoring and compliance traceability. Those buyers absorb rate pressure through contract renegotiation; they don’t cancel outright.

Laos attracts a different order-book profile: smaller volumes, more price-sensitive buyers, often seeking cost arbitrage rather than supply chain partnership. That type of order evaporates first when the cost-advantage calculation shifts. At $1.38 diesel per litre, 9% inflation, and contested power supply, the cost arbitrage over Cambodia is narrowing faster than most 2025 order forecasts assumed. The buyers most exposed to that narrowing — those who moved Laos allocations up in late 2025 chasing the railway story — are the ones now running revised landed-cost calculations that may not close.

What H1 2027 looks like from here #

The resolution of these pressures points in divergent directions over the next 12 months.

Cambodia’s freight problem is seasonal. Monsoon season passes in October-November. Global container rates will likely moderate from their current peak as carrier capacity adjusts. The EERF energy savings begin to accrue for factories that access the fund; the customs reform, if it progresses, reduces dwell-time friction by mid-2027. The July 5 border incident, unless it escalates, will fade from the logistics risk register. Cambodia’s trajectory in this cycle is: disruption now, structural improvement later.

Laos’ trajectory is the inverse. The fuel cost increase is permanent until the next emergency cut. EDL’s fiscal restructuring is a multi-year programme. Inflation at 9% does not resolve in a quarter. The kip depreciation trend is not reversing on Cambodia’s timetable. The railway’s full impact on export routing — specifically, whether Hai Phong can become a viable export gateway for Laos-made garments via upgraded inland logistics — is a five-year story, not a 2026 answer.

The asymmetric conclusion, for a sourcing manager making Q4 bets in July 2026: Cambodia’s lead time uncertainty is temporary; Laos’ cost-advantage erosion is structural. That is not the obvious read when Cambodia’s freight problems are visible and Laos’ railway headlines are still positive. But it is the correct one for H1 2027 planning.

The factories that understand the difference between a resupply advantage and a delivery advantage will position their order books accordingly. The ones that don’t will learn the distinction from their Q4 landed-cost reports.

References:

- Phnom Penh Post (2 Jul 2026). “ADB-backed $20m fund looks to cut energy costs, boost competitiveness for Cambodian SMEs.” https://phnompenhpost.com/business/adb-backed-20m-fund-looks-to-cut-energy-costs-boost-competitiveness-for-cambodian-smes/ (Accessed 7 Jul 2026)

- Phnom Penh Post (30 Jun 2026). “Government invites private sector input on new customs regulations.” https://phnompenhpost.com/business/government-invites-private-sector-input-on-new-customs-regulations/ (Accessed 7 Jul 2026)

- Phnom Penh Post (6 Jul 2026). “Cambodia investigates border blast that injured four soldiers; Thailand denies involvement.” https://phnompenhpost.com/national/cambodia-investigates-border-blast-that-injured-four-soldiers-thailand-denies-involvement/ (Accessed 7 Jul 2026)

- Laotian Times (26 Jun 2026). “Laos Restores Higher Fuel Excise Taxes as Emergency Relief Measures End.” https://laotiantimes.com/2026/06/26/laos-restores-higher-fuel-excise-taxes-as-emergency-relief-measures-end/ (Accessed 7 Jul 2026)

- Laotian Times (4 Jul 2026). “Vietnam, Philippines Reach Upper-Middle-Income Status as Laos Eyes 2035 Target.” https://laotiantimes.com/2026/07/04/vietnam-philippines-reach-upper-middle-income-status-as-laos-eyes-2035-target/ (Accessed 7 Jul 2026)

- FreightWaves (30 Jun 2026). “Wartime economy: Maersk lifts full-year guidance on strong demand.” https://www.freightwaves.com/news/wartime-economy-maersk-lifts-full-year-guidance-on-strong-demand (Accessed 7 Jul 2026)

- Drewry Supply Chain Advisors (2 Jul 2026). “World Container Index — 2 Jul.” https://www.drewry.co.uk/supply-chain-advisors/supply-chain-expertise/world-container-index-assessed-by-drewry (Accessed 7 Jul 2026)

- The Nation Thailand (30 Jun 2026). “DDPM warns of flash floods as heavy rain hits Thailand.” https://www.nationthailand.com/news/general/40068064 (Accessed 7 Jul 2026)

- SEAWeekly / P’Chai Srisuk (1 Jul 2026). “What’s driving Thailand port congestion risk ahead of peak monsoon shipping season?” https://seaweekly.com/posts/2026-07-01-thailand-port-congestion-monsoon-shipping-season/ (Accessed 7 Jul 2026)

- SEAWeekly / Nguyen Minh An (10 Jun 2026). “What’s driving Laos energy import costs and inflation pressure in 2026?” https://seaweekly.com/posts/2026-06-10-laos-energy-import-costs-inflation-pressure/ (Accessed 7 Jul 2026)

- SEAWeekly Port Congestion Brief (9 Jun 2026). “ASEAN Port Congestion: The Bifurcated Peak Season Story.” https://seaweekly.com/posts/2026-06-09-asean-port-congestion-brief/ (Accessed 7 Jul 2026)