The economy page tracks growth momentum, trade performance, inflation-sensitive consumer trends, and the business implications of regional demand shifts. Southeast Asia as a bloc is one of the world’s fastest-growing economic zones, with collective GDP surpassing USD 3.6 trillion and intra-regional trade deepening through RCEP and bilateral agreements. Coverage connects macro signals — GDP prints, current-account moves, currency pressure — to the ground-level commercial decisions they drive across the ten ASEAN member states.

Regional GDP: ASEAN collective output exceeds USD 3.6 trillion, ranking it among the world’s top five economic blocs

Growth leaders: Vietnam, Philippines, and Indonesia have consistently posted among the fastest GDP growth rates in the Asia-Pacific

Trade framework: The Regional Comprehensive Economic Partnership (RCEP) covers roughly 30 % of global GDP and shapes tariff exposure for every exporting nation in the region

Consumer base: A combined population of ~680 million, with a middle class projected to reach 350 million by 2030, underpins rising domestic demand

Inflation sensitivity: Food and fuel price movements carry outsized weight in household budgets, making CPI and commodity data closely watched editorial signals

Singapore is winning ASEAN capital-flow positioning because Brunei has hard-currency credibility and sovereign wealth, but not the intermediation layer global money pays for.

Laos is becoming more important to ASEAN’s power grid, but export scale alone will not repair the balance sheet unless Laos captures more value from transmission, PPAs, and domestic grid reform.

Thailand is actively raising prices across airlines and hotels and demand holds. The Philippines’ high per-visitor yield is a supply constraint, not a strategy — and the distinction is the most important signal in ASEAN tourism right now.

This week’s ASEAN signal is not about growth; it is about systems integration — the markets where fintech infrastructure and industrial throughput are closing into a single investable stack are attracting better capital, on better terms, than those where the two layers are still moving on separate calendars.

Philippine aviation demand is surging but infrastructure constraints and visa barriers mean the benefits are increasingly captured by ASEAN competitors with better capacity to serve high-yield travellers.

Vietnam’s export recovery is real, but logistics costs at 16–20% of GDP mean every freight-rate swing hits exporters harder here than anywhere else in ASEAN — and the US-Iran peace deal won’t deliver a clean cost reset.

Timor-Leste has ASEAN membership, a credible sovereign wealth fund, and a functioning PPP — the question is whether these can attract sufficient private capital before the Petroleum Fund depletion timeline binds.

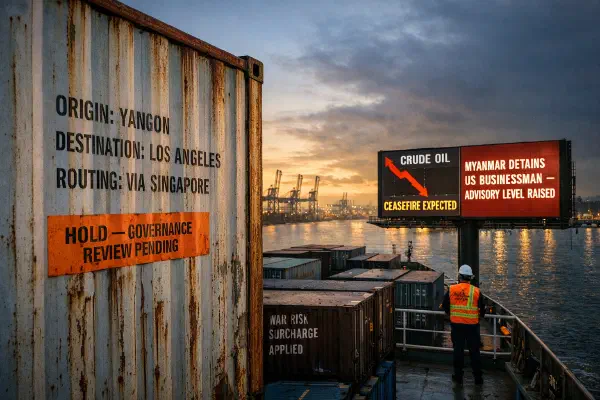

The US-Iran peace deal is the best supply chain news ASEAN frontier markets have had all year. But governance risk is now repricing upward on its own axis, and the net premium may not fall as much as logistics alone would suggest.

Brunei is taking the right institutional steps toward post-hydrocarbon diversification, but the pieces aren’t yet connected, the sovereign wealth lever remains under-deployed, and the Iran war windfall is both the best enabler and the biggest trap.

ASEAN’s fiscal divergence in 2026 is not primarily about who exports oil. It’s about who made subsidy reform calls in the quiet years before the shock — and Malaysia and the Philippines are holding more fiscal cards going into H2 than Indonesia or Thailand.

Laos inflation is running at 9% because the country is structurally pinned: it produces 83% of its energy from hydropower yet cannot keep Électricité du Laos solvent, and it has zero domestic refining capacity yet imports 97% of its fuel from Thailand.

Southeast Asia’s garment sector is facing a reckoning where the savings of low-cost manufacturing are being erased by “Logistics Entropy”—the combined cost of surging fuel, worker safety crises, and unpredictable US trade policy. Cambodia is repositioning as a “stable but expensive” hub, while Myanmar is increasingly viewed as a “no-go” zone for all but the most risk-tolerant.