Indonesia is Southeast Asia’s largest economy and the world’s fourth most populous country, with around 280 million people spread across more than 17,000 islands. Its commodity wealth — nickel, palm oil, coal, and copper — underpins a resource-processing industrial base, while a fast-growing domestic consumer market and vibrant fintech sector are reshaping finance and retail. Jakarta remains the primary business hub ahead of a phased capital relocation to Nusantara in East Kalimantan, and the archipelago’s diversity fuels one of the region’s most compelling travel propositions.

This week’s ASEAN signal is not about growth; it is about systems integration — the markets where fintech infrastructure and industrial throughput are closing into a single investable stack are attracting better capital, on better terms, than those where the two layers are still moving on separate calendars.

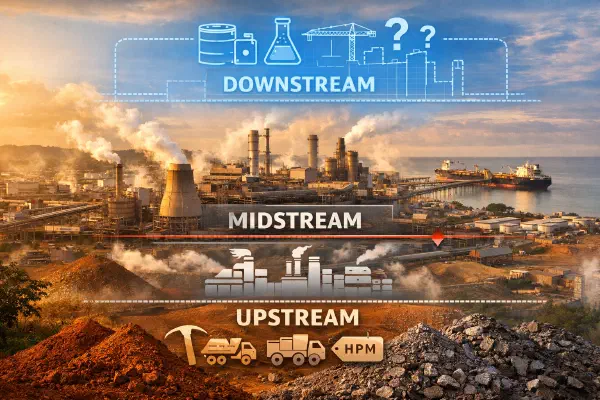

Indonesia’s nickel value capture in 2026 is not a single story of triumph or capture — it is a three-layer contest between the state, Chinese processors, and new entrants, and each layer has a different winner.

ASEAN loan growth numbers are hiding a deeper liquidity stress in the deposit base — and when liquidity tightens, loan growth is the last metric to turn.

Singapore’s institutional premium model and Malaysia’s consumer ecosystem model represent two fundamentally different answers to the same question — how to turn digital payments ubiquity into profit — and the gap between them is reshaping fintech strategy across ASEAN.

Timor-Leste has ASEAN membership, a credible sovereign wealth fund, and a functioning PPP — the question is whether these can attract sufficient private capital before the Petroleum Fund depletion timeline binds.

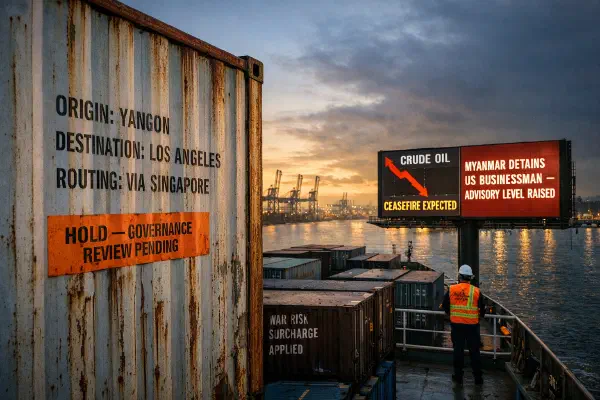

The US-Iran peace deal is the best supply chain news ASEAN frontier markets have had all year. But governance risk is now repricing upward on its own axis, and the net premium may not fall as much as logistics alone would suggest.

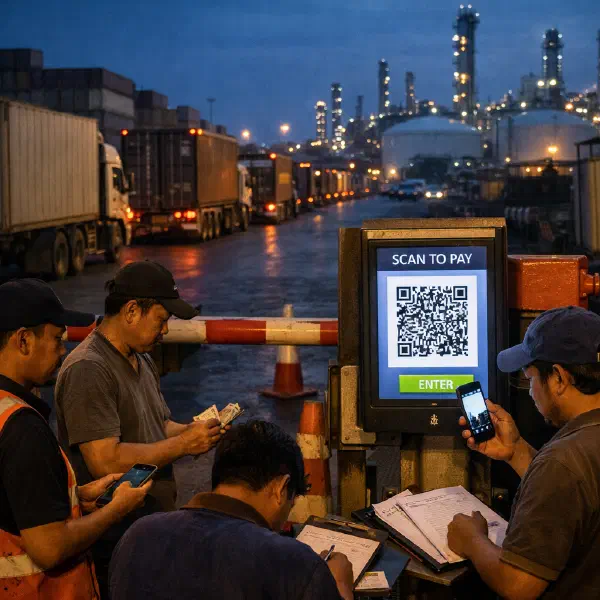

Indonesia’s banks are in their best-ever shape, but rupiah defense is creating a credit transmission failure that will define ASEAN lending patterns through H2 2026.

ASEAN’s fiscal divergence in 2026 is not primarily about who exports oil. It’s about who made subsidy reform calls in the quiet years before the shock — and Malaysia and the Philippines are holding more fiscal cards going into H2 than Indonesia or Thailand.

The key ASEAN shift this week is not whether money is coming in, but where it is willing to stay. Investors are concentrating on execution-dense, policy-credible growth nodes and treating the rest of the region as higher-carry exposure.

The manufacturing contest between Indonesia and Vietnam is no longer about picking one winner. Vietnam remains the faster export platform; Indonesia is gaining importance as a hedge for tariffs, resources, and upstream scale. The smarter ASEAN supply-chain strategy now assigns each country a different role.

This week’s signal across ASEAN is clear: growth headlines matter less than who can absorb FX, energy, and working-capital shocks while still compounding capability.