The Philippines is an archipelago of more than 7,600 islands with a population approaching 115 million, making it the second most populous country in Southeast Asia. Its business process outsourcing industry generates billions of dollars in annual revenue and supports a large urban middle class, while overseas remittances — one of the highest in the world relative to GDP — drive consumer spending and financial inclusion. Island tourism across Palawan, Cebu, and Siargao is growing quickly, and basketball’s extraordinary popularity creates a uniquely deep sports media economy.

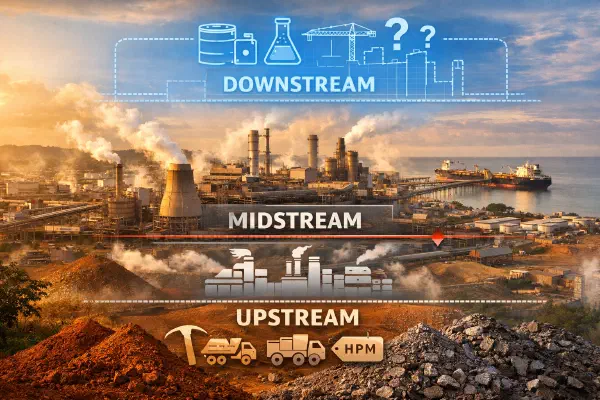

Indonesia’s nickel value capture in 2026 is not a single story of triumph or capture — it is a three-layer contest between the state, Chinese processors, and new entrants, and each layer has a different winner.

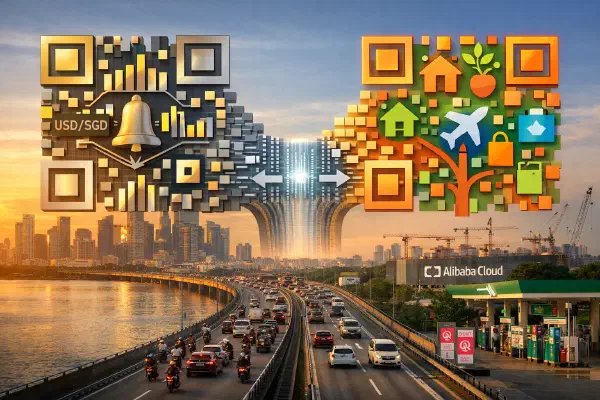

Singapore’s institutional premium model and Malaysia’s consumer ecosystem model represent two fundamentally different answers to the same question — how to turn digital payments ubiquity into profit — and the gap between them is reshaping fintech strategy across ASEAN.

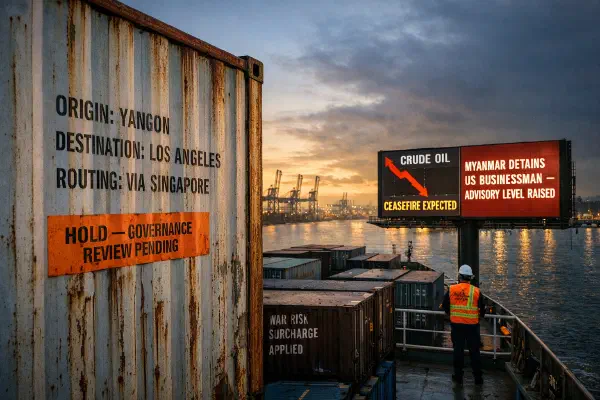

The US-Iran peace deal is the best supply chain news ASEAN frontier markets have had all year. But governance risk is now repricing upward on its own axis, and the net premium may not fall as much as logistics alone would suggest.

ASEAN’s fiscal divergence in 2026 is not primarily about who exports oil. It’s about who made subsidy reform calls in the quiet years before the shock — and Malaysia and the Philippines are holding more fiscal cards going into H2 than Indonesia or Thailand.

Record remittance volumes mask a quality story that matters far more for Philippines household consumption in 2026 — the sectoral and geographic composition of OFW sending patterns is quietly reshaping what families can actually spend.

This week’s biggest Southeast Asia stories show a region attracting capital at scale while still struggling to keep enough value, capability, and resilience at home.

Southeast Asia’s biggest economic stories this week share one pattern: governments are no longer just inviting capital — they are redesigning where margins sit.

Prabowo’s 8% commission cap is a labor story on the surface. Underneath it is a systematic nationalization of value capture in Indonesia’s platform economy — and Danantara’s dual role as owner and regulator is the most consequential development in SEA tech this year.

Three signals from one week: Vietnam becomes SEA’s first country with a binding AI law, Money20/20’s APAC report declares the region has moved from pilots to production, and the UBS OneASEAN Summit puts 4.9% GDP growth on the record.

DBS-Visa AI agent payments, the Philippines’ dual IPO race, and Indonesia’s new digital innovation hub all point to the same quiet shift: Southeast Asia is building financial infrastructure, not just fintech apps.