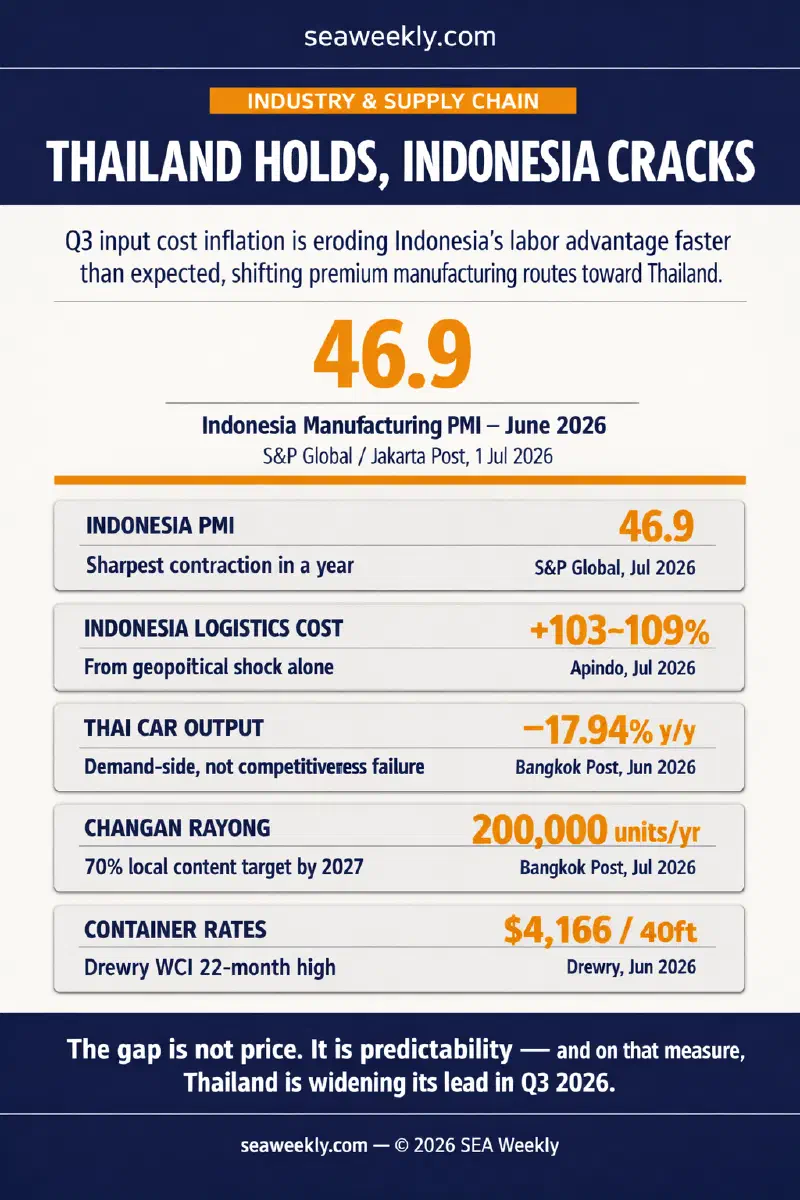

Two pieces of data, released ten days apart, define the Thailand-Indonesia manufacturing competition in Q3. On June 29, Bangkok Post confirmed Thai car production fell 17.94% year-on-year in May — a fifth consecutive monthly decline in the sector that built Thailand’s industrial identity. On July 1, S&P Global reported Indonesia’s manufacturing PMI plunged to 46.9, the sharpest contraction in a year, with export orders falling at the steepest pace since August 2021. Both stories read as manufacturing distress. But the signature underneath each number is different — and that difference is now driving Q3 supply chain routing decisions.

When Two Contractions Tell Different Stories #

Thailand’s automotive production decline is real. The Federation of Thai Industries has set a 2026 production target of 1.5 million vehicles — 950,000 for export and 550,000 for the domestic market — and the industry’s own spokesman has warned the export target may be missed due to Middle East geopolitical tensions. (Bangkok Post, 29 Jun 2026) The cause is not hard to identify: Thailand’s household debt has reached 13.6 trillion baht, non-performing loans are running at 9.3%, and auto loans have become harder to obtain as the credit environment tightens. (Nation Thailand, 30 Jun 2026) This is demand destruction, not a manufacturing competitiveness failure.

Indonesia’s June PMI tells a structurally different story. The 46.9 reading — down from 50.0 in May, the threshold between expansion and contraction — was driven by input price inflation accelerating to its most pronounced level since September 2013, which the survey described as the second-highest rate in its history. (Jakarta Post, 1 Jul 2026) New export orders fell at the steepest pace since August 2021 — not because buyers withdrew demand, but because Indonesian goods became less price-competitive in international markets as costs compounded. Production has now contracted for four consecutive months. Job shedding reached its most severe level since September 2021.

Two contractions. One demand-side, one cost-push. The distinction matters for where supply chain routing goes.

Thailand’s Higher-Cost, Higher-Reliability Model #

The announcement that cuts through the noise came on July 13. Hyundai confirmed it will export Thailand-manufactured battery electric vehicles to Australia. (Bangkok Post, 13 Jul 2026) This is not an incentive capture play. This is a routing decision: a Korean automaker selecting Thailand as its production-to-export hub for a demanding right-hand-drive market with strict standards. While every analyst is reading Thailand’s production decline as competitiveness retreat, Hyundai is doing the opposite — using Thailand as a premium export base.

The Changan story tells the same version of the argument. Changan Auto Sales Thailand vice president Chris Wu has publicly committed the company to increasing local sourcing of EV component costs to 70% by 2027 and 80% by 2030 — well above the current requirements under the EV3.5 scheme — with a 10-billion-baht Rayong facility targeting 200,000 units per year. (Bangkok Post, 13 Jul 2026) Changan is already exporting to right-hand-drive markets including the UK from that facility. Its “Global Vast Ocean” strategy positions Thailand as its primary export hub outside China.

These decisions are not policy-compliant box-ticking. Companies that absorb Thai Tier 1 suppliers into their global supply structure are building the kind of ecosystem depth that survives a single-quarter production downturn. The mechanism is the same one that built Japan’s auto ecosystem in the 1980s, China’s electronics ecosystem in the 2000s, and now Thailand’s EV supply chain in the 2020s — consistent capital commitment in a reliable regulatory and logistics environment, compounded across years, becomes sticky advantage.

The port logistics backdrop completes the picture. Laem Chabang is handling queuing premiums of $50-150 per container before the monsoon season even arrives, running at near-maximum design capacity for three years. (SEAWeekly, 1 Jul 2026) That is expensive. But it is a known, plannable cost. Supply chain managers building annual routing budgets can model $150 per container. What they cannot model is a cost that has doubled without warning.

Indonesia’s Cost-Push Signature #

The Indonesian Employers Association put a number on the shock in early July. Reporting to the Quarantine Agency on the logistics cost environment, Apindo stated that the US-Israel war on Iran had pushed logistics costs up by 103 to 109 percent. (Jakarta Post, 2 Jul 2026) That is not a freight rate increase. It is a freight rate doubling, sitting on top of input price inflation at a 13-year high. When logistics costs double, the competitive advantage of a lower minimum wage is consumed in transit.

The structural tension is visible in an analysis published by the Jakarta Post the following week: Indonesia’s economy expanded 5.61% in Q1 2026, with government expenditure surging more than 21%. But manufacturers were telling a different story — factory orders shrinking, export demand weakening, production slowing, firms cutting headcount at the most severe pace since September 2021. (Jakarta Post, 8 Jul 2026) The decoupling of GDP from manufacturing is not a rounding error. It reflects the structural gap between an economy running on government stimulus and a manufacturing base under cost-push pressure that government spending does not directly relieve.

Consumer confidence has followed the manufacturing PMI downward. Bank Indonesia’s Consumer Confidence Index fell to 117.8 in June from 120.9 in May, approaching the multiyear low of 115 registered last September. (Jakarta Post, 9 Jul 2026) Indonesian factory workers feeling input price inflation through eroding purchasing power are the same cost environment that makes their employers’ export products uncompetitive in international markets. The pressure is consistent across both the factory gate and the household.

Q3 Routing: The Predictability Premium #

Supply chain routing decisions in Q3 are being made against the backdrop of Drewry’s World Container Index reaching $4,166 per 40-foot container — a 22-month high — with further increases signalled by carriers for July. At those rate levels, every routing decision is expensive. The question is not which corridor is cheap. The question is which corridor’s costs are predictable.

Thailand’s answer in Q3 is: Laem Chabang’s congestion premium is active and documented. It can be priced. Indonesia’s answer in Q3 is: logistics costs have more than doubled from geopolitical shock, regulatory checkpoints between Jakarta and regional offices create unpredictable interpretation differences, and the industry council that might fix this structural problem is still being drafted. The predictability gap is not a marginal edge. In Q3 conditions, it is the routing decision.

For electronics and EV/auto supply chains — the categories where production volumes justify the premium-corridor calculation — Thailand is capturing the routing decision. The Hyundai Australia destination is not a coincidence in this analysis; it is the outcome of that calculation at scale.

Marcus’s take: The Indonesia read requires two caveats that the routing analysis tends to miss. First: S&P Global affirmed Indonesia’s sovereign credit rating at BBB with a stable outlook on July 13. (Jakarta Post, 13 Jul 2026) This is not a country in structural distress. The Q3 manufacturing cost shock is real and severe, but it is cyclical-plus-policy stress, not terminal decline. Second: Indonesia’s manufacturing disadvantage in Q3 is not the same as Thailand’s manufacturing advantage being durable beyond 2027. Thailand’s EV3.5 incentive scheme expires next year, and the Federation of Thai Industries is explicitly warning that without a replacement, Chinese manufacturers may revert to importing under ASEAN-China FTA zero tariffs. (Bangkok Post, 13 Jul 2026) The routing advantage that Hyundai and Changan represent is conditional on policy continuity — something BOI has historically delivered, but cannot be assumed.

Indonesia’s own reform trajectory has the right direction. Danantara’s move to merge seven state-owned logistics enterprises is the structural answer to the supply chain inefficiency that my earlier analysis documented across the nickel downstream corridor — and it applies equally to the broader manufacturing sector. (SEAWeekly, 3 Jul 2026) The new industry council, if it acquires real authority to cut permit timelines, addresses the investment-limiting regulatory complexity that the HKI has flagged for years. Neither reform is operational in time for Q3 routing decisions. But both are signals that Jakarta has diagnosed the right disease. The question is whether the treatment arrives before the patient reassigns its supply chain contracts.

The 18-Month Test #

The Q3 routing picture is a moment, not a permanent verdict. Thailand’s manufacturing position is advantaged today — and is testing its durability through the EV3.5 sunset cycle. If the BOI produces a credible replacement scheme, and if Chinese automakers like Changan follow through on their localisation commitments regardless of incentive structure, Thailand’s supply chain ecosystem becomes a genuine structural moat. If EV3.5 expires without replacement, the routing advantage is a policy artifact, not a competitive one.

Indonesia’s position is stressed today — and is testing whether its reform pace can close the reliability gap before the next wave of ASEAN manufacturing FDI is locked in. The B50 biodiesel mandate rolled out this week adds one more input cost layer in the short term. (Jakarta Post, 10 Jul 2026) Danantara’s logistics merger and the industry council both point in the right direction over a 12-24 month horizon. But ASEAN supply chain buyers making routing commitments for H2 and into 2027 are making those decisions right now.

The winner of the next ASEAN manufacturing cycle will not be determined by which country has the lower headline wage rate. It will be determined by which country can credibly promise that a finished goods container placed on a vessel today will arrive at its destination on a predictable schedule, at a cost that was modelled in the procurement spreadsheet, not discovered at the port gate. Thailand holds that promise in Q3 2026. The 18-month question is whether Indonesia can retake it.

References:

- Bangkok Post (29 Jun 2026). “Automotive sector posts downturn in first 5 months.” https://www.bangkokpost.com/business/motoring/3278539/automotive-sector-posts-downturn-in-first-5-months (Accessed 14 Jul 2026)

- Nation Thailand (30 Jun 2026). “Thailand’s 13.6tn-baht debt problem moves into small loans.” https://www.nationthailand.com/business/economy/40068050 (Accessed 14 Jul 2026)

- Jakarta Post (1 Jul 2026). “RI factories slide into contraction in June amid soaring costs, weak demand.” https://www.thejakartapost.com/business/2026/07/01/ri-factories-slide-into-contraction-in-june-amid-soaring-costs-weak-demand (Accessed 14 Jul 2026)

- Jakarta Post (2 Jul 2026). “Businesses urge easing of quarantine rules amid rising logistics costs.” https://www.thejakartapost.com/business/2026/07/02/businesses-urge-easing-of-quarantine-rules-amid-rising-logistics-costs (Accessed 14 Jul 2026)

- Jakarta Post (8 Jul 2026). “When economic growth and manufacturing go their separate ways.” https://www.thejakartapost.com/opinion/2026/07/08/when-economic-growth-and-manufacturing-go-their-separate-ways (Accessed 14 Jul 2026)

- Jakarta Post (9 Jul 2026). “Consumer confidence, retail sales dip further after rate hikes.” https://www.thejakartapost.com/business/2026/07/09/consumer-confidence-retail-sales-dip-further-after-rate-hikes (Accessed 14 Jul 2026)

- Jakarta Post (10 Jul 2026). “New industry council risks more rhetoric than reform.” https://www.thejakartapost.com/business/2026/07/10/new-industry-council-risks-more-rhetoric-than-reform (Accessed 14 Jul 2026)

- Jakarta Post (10 Jul 2026). “Indonesia rolls out B50 biodiesel mandate, lifting palm oil demand.” https://www.thejakartapost.com/business/2026/07/10/indonesia-rolls-out-b50-biodiesel-mandate-lifting-palm-oil-demand (Accessed 14 Jul 2026)

- Jakarta Post (13 Jul 2026). “S&P affirms BBB rating, stable outlook for Indonesia.” https://www.thejakartapost.com/business/2026/07/13/sp-affirms-bbb-rating-stable-outlook-for-indonesia (Accessed 14 Jul 2026)

- Bangkok Post (13 Jul 2026). “Content fight shapes Thailand’s EV future.” https://www.bangkokpost.com/business/motoring/3285207/content-fight-shapes-thailands-ev-future (Accessed 14 Jul 2026)

- Bangkok Post (13 Jul 2026). “Hyundai to export Thai BEVs to Australia.” https://www.bangkokpost.com/business/motoring/3285127/hyundai-to-export-thai-bevs-to-australia (Accessed 14 Jul 2026)

- Drewry (25 Jun 2026). World Container Index. https://www.drewry.co.uk/supply-chain-advisors/supply-chain-expertise/world-container-index-assessed-by-drewry (Accessed 1 Jul 2026)