Episode 20: Why ASEAN Logistics and Freight Signals Are Emerging as the New Leading Indicators for H2 Growth

·3131 words·15 mins

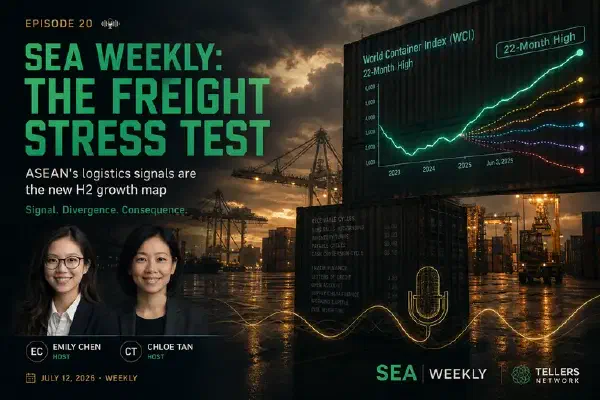

The Drewry World Container Index hit four thousand six hundred and thirty-nine US dollars per forty-foot container on July 9 — the highest since September 2024. Two days earlier, the ADB lowered its 2026 growth forecast for developing Asia to four-point-nine percent. Chloe Tan joins Emily Chen to work through why those two numbers are measuring the same economy, but one arrived weeks ahead of the other — and why the freight signal, not the GDP revision, is the more useful H2 guide.